Categories for

What Does the Metaverse Mean for Businesses

Metaverse has become a buzzword with much debate on its potential implications once it is fully realized. As far as businesses are concerned, the metaverse presents new opportunities and challenges, especially for marketing, branding, and communication professionals.

Understanding Metaverse

Metaverse became a hot topic thanks to Facebook announcing its rebrand to Meta in October 2021. However, the metaverse is not new and can be traced back to 1992 in the fiction novel “Snow Crash” by Neal Stephenson. Stephenson used the term to refer to a virtual world where people can do different activities.

As the internet moves to a new iteration as Web 3.0, different players are working toward creating their metaverse – or rather, a unified virtual space. This virtual environment is intended to be used to carry out activities such as playing games, attending meetings, buying digital goods and services, conducting tourism, getting education, and even for working.

Although metaverse might seem like a futuristic notion that will require massively advanced technologies, its foundational elements are already in place. This is because it’s enabled by virtual reality (VR) and augmented reality (AR). Some users, especially gamers, have had experiences with virtual reality and augmented technologies. Some online retailers already use augmented reality on their e-commerce platforms to help shoppers experience a product before ordering it.

However, metaverse technology seeks to connect all of these separate apps and platforms to create a continuous experience that will integrate audiences and elements from different platforms into one. The metaverse will be characterized by a boundless and decentralized virtual economy and immersive social experiences.

It is not possible yet to gauge how disruptive the metaverse will be, but one sure bet is that it will introduce new ways of doing things. As has already been witnessed, to keep up with trends, businesses had to adapt to technologies such as social media platforms even when they were initially created for social interaction. Hence, businesses need to be prepared.

Metaverse in Business

As any new technology helps early adopters gain a significant advantage over competitors, metaverse will be no different. However, it may initially favor large businesses that can afford to take risks and have budgets to invest in enabling requirements. Despite this, different-sized businesses should get ready to adjust their marketing strategies to the virtual economy.

There are predictions that the metaverse could generate vast revenue to the tune of $1 trillion. Hence, the metaverse has a massive business opportunity, including advertising, demand for new hardware, virtual events, e-commerce, etc.

As an example of the readiness for companies to adopt metaverse, consider Nike. The brand has already taken steps into the metaverse by filing for trademark applications indicating its intention to make and sell virtual branded sneakers and apparel.

Businesses will benefit differently from the metaverse. For instance, companies manufacturing computer chips and servers stand a good chance for a significant gain to their businesses. So will cloud service providers that will be vital for the metaverse virtual worlds.

Manufacturers also will use the metaverse to create digital models of their products using digital twins technology (a virtual representation of a physical object or process). This will help adjust manufacturing processes, carry out quality control, product demos, and simulate the supply chain.

Remote work that was highly adopted due to the recent pandemic will be enhanced by the metaverse. It will be possible to have co-working spaces and carry out virtual training and simulations.

It also will help promote physical businesses. By interacting with objects in 3D form, shoppers can try on clothes online, check out houses, cars, etc. The ability to shop virtually means that businesses can design brands to suit different customer needs and increase retail sales.

Such possibilities mean that marketers will need to research customer behavior and preferences in the virtual space. This will require businesses to set up metaverse teams if they want to remain competitive. This is especially necessary to reach customers where they spend their time.

On the downside, there are concerns about privacy issues and data harvesting – like any other technology. The decentralized characteristic of a true metaverse also means it will be challenging to regulate. Such cases introduce risks to businesses. Nevertheless, such risks have never stopped businesses from adopting new technologies.

Conclusion

Customer experience is vital in any business. For businesses to continue maintaining long-term relationships with customers, they may have to adapt and use virtual avatars to serve as customer service agents. Thus, businesses need to be more innovative to tie existing communication channels to the metaverse channel. They can do this by formulating an entry plan to the metaverse while ensuring a balance between opportunities and risks.

How Soon and Fast Will the Fed Raise Rates?

There’s much uncertainty surrounding if, how, and when the Federal Reserve will raise its rates, end its bond and mortgage-backed security purchases, and wind down its balance sheet. For the March 16 Fed Meeting, the CME FedWatch Tool has a 47.9 percent probability of a 25 to 50 basis point increase and a 52.1 percent probability of a 50 to 75 basis point increase for their Target Rate. There are many expectations for the Fed to raise its Federal Funds rate, or the so-called overnight lending interbank rate. However, there’s a lot of uncertainty as to how many times the FOMC will increase it.

John Williams, Federal Reserve Bank of New York president, mentioned at a recent event that the Federal Open Market Committee (FOMC) will start raising rates at its March 2022 meeting, but he isn’t advocating for a particularly hawkish approach. Rather, Williams expects inflation to drop due to supply-chain bottlenecks being naturally worked out, along with the Fed’s measured policy actions moderating inflation. However, James Bullard, Federal Reserve Bank of St. Louis president, is more hawkish and has expressed a desire for a 50 basis point rate hike.

Lael Brainard, a member of the Federal Reserve’s Board of Governors, believes six rate hikes are an appropriate course for monetary policy, starting in March 2022. Charles Evans, Chicago Fed president, blames inflation on the pandemic and echoes that supply chain issues will resolve on their own as the world returns to its new normal. Evans also believes that hiring won’t be slowed with higher rates, compared to past rate hike cycles. However, this could change if inflation grows too high as 2022 progress, necessitating more rate hikes.

The Fed has communicated clearly that it will let 1) evolving economic data, in conjunction with 2) maximum employment, and 3) 2 percent longer-term inflation expectations guide its monetary policy. Noting there’s been a strengthening labor market, it’ll continuously look at how the pandemic is managed healthwise, how global developments unfold, and how inflation is expected to end materializes.

It’s important to note that during August 2020, the Fed took a new approach to inflation. Previously, the approach was to increase borrowing rates during good economic times to prevent inflation from becoming a problem. However, as of August 2020, the Fed’s new approach is to maintain low rates until inflation materialized, permitting economic conditions that drive inflation above and below 2 percent. This would thereby create a longer-term average inflation rate of 2 percent when considering monetary policy adjustments.

This is within the perspective of inflation reaching 7.5 percent year-over-year in January 2022, according to the Labor Department. Month-over-month inflation readings include electricity rising 4.2 percent from December 2021 to January 2022. Food costs rose by 0.9 percent in January 2022, up from another 0.5 percent increase in December 2021.

According to the FOMC’s Jan. 26 meeting minutes, there’s much to be contemplated for any potential rate changes. The members found that inflation was elevated, with economic indicators showing inflationary pressures increased in the back half of 2021. In December, the 12-month change in the consumer price index (CPI) was 7 percent, while core CPI inflation was 5.5 percent over the same period.

The year-over-year November 2021 total personal consumption expenditures (PCE) price inflation was 5.7 percent, with the core PCE coming in at 4.7 percent for the same timeframe. When it comes to the unemployment rate, it fell from 4.2 percent in November 2021 to 3.9 percent in December.

Impact of Russia-Ukraine Conflict

Looking at the price of crude oil alone shows how inflation is fluctuating. On Feb. 24, futures contracts at one point had oil hitting $100 and $105 per barrel for West Texas Intermediate and Brent, respectively. While prices retreated, prices are still elevated and subject to international tensions, increasing demand due to the economy reopening from COVID, and uncertainty over future output. Undoubtedly, the Fed will take inflation into account – both its new definition of longer-term 2 percent inflation and how it might impact the economy. Some speculate with the high volatility beginning in 2022, the Fed may raise rates by only 25 basis points, not the 50 basis points more hawkish FOMC members have mentioned.

With increased volatility since 2022 began and global uncertainty increasing by the day, it seems the FOMC will have the final say on how many rate hikes will eventually happen.

Congratulations, You Just Sold Your Business: What Happens Next?

One of the most important things to understand about selling a business is that this is not a decision that should be made lightly.

This is true both in terms of who you sell to and with regard to what will happen to your finances after all is said and done. You need a solid financial plan in place ahead of time to not only make the most of the sale, but to guarantee that you’ll have everything you need to live as comfortably as possible moving forward.

The Art of Selling Your Business

By far, the most important step that you can take in terms of selling your business actually occurs before the sale even happens: planning ahead.

When you sell your organization, especially if you’re lucky enough to do so for millions of dollars, you generate enough of a profit to live comfortably for several years. But you need to be forward-thinking in terms of how you maximize those profits with regard to the taxes you’ll be required to pay.

A great strategy for long-term investors is QSBS stock exclusion, which permits shareholders of certain qualified small businesses to exclude a significant portion or all their associated capital gains when selling or exchanging that stock if they’ve held it over five years.

The point is that you’re maximizing the income that you’re actually making from the sale of your company, which ultimately should be the goal of any entrepreneur. So planning ahead can literally save you millions in tax liability and higher take-home cash. QSBS is just one example of possible tax strategies.

Another critical step to take after selling your business involves evaluating all healthcare options available to you. In a lot of situations, entrepreneurs will sell their company prior to the age of 65 — meaning before they are eligible for Medicare. Depending on the nature of the sale, they may be able to stay on a company-sponsored health insurance plan. They may also be able to get coverage through a spouse who is still employed. But if neither of these things is true, they’re likely going to need to find coverage on the open market — something that can amount to thousands of dollars every year.

This is why working with insurance brokers and other financial professionals is key because it can help make sure your health insurance needs are taken care of within the context of the impending business sale. It’s critically important to think about this if you also have a chronic health condition like diabetes. It may not seem like a big expense prior to the sale, but health conditions come with doctor’s visits, expensive prescriptions, etc. You need to make sure that you’re not being short-sighted — that you’re getting the necessary care you need while still maximizing the profits from the sale at the exact same time.

Finally, when it comes to taxes, it’s also important to look at a charitable donation strategy — especially if you’ll be cashing in company stock as you exit the business entirely. Making a significant charitable donation during the same year in which you sell your company is hugely beneficial as it can help counteract much of the regular income taxes that you would be forced to pay as a result of the transaction.

In the end, selling a business is never an easy decision. You’ve devoted a significant portion of your life to building something special — parting with it is always going to be difficult. But from the financial side of the equation, so long as you follow a few key best practices, you’ll be able to enjoy all of the benefits of this process with as few of the potential downsides as possible.

If you’d like to find out more information about what happens in the wake of selling your business, or if you just have any additional questions that you’d like to go over with someone in a bit more detail, please don’t delay — contact us today.

Return Being Processed Means the IRS Received Your Tax Return, But It Could Still Be Delayed

Many taxpayers use the Where’s My Refund tool and wonder what “Return being processed” means for them and their refund.

The answer: not much yet!

The prompt means that the IRS has received your return, but due to Covid-19 delays, the IRS is experiencing a considerable backlog, slowing processing times and disbursements.

Typically the IRS processes tax returns and issues refunds within 21 calendar days of receipt. The IRS even stated in January communicating the 21-day time frame.

Add in the pandemic-related tax changes and child tax credit advances, and this tax season is more complicated than ever.

Avoid filing a paper return.

Use electronic filing with direct deposit to receive your tax refund the fastest way.

If your tax refund is delayed, you have options.

You can call the IRS, but you should wait out the delays before putting yourself through this added stress. Due to the backlog, it can take 6-8 weeks to process your tax return.

The following are some of the reasons why tax returns take longer than others to process:

- Your tax return includes errors, such as incorrect Recovery Rebate Credit

- Your tax return Is incomplete

- Your tax return needs further review in general

- Your tax return Is affected by identity theft or fraud

- Your tax return includes a claim filed for an Earned Income Tax Credit or an Additional Child Tax Credit

- Your tax return consists of a Form 8379, Injured Spouse Allocation, which could take up to 14 weeks to process

How to contact the IRS

You may call 800-829-1040 with any Federal tax questions.

Getting through to the IRS over the phone is a challenge. According to the Taxpayer Advocate, only 1 in 9 calls to the IRS are answered. This even with a long wait time.

Not surprisingly, it is best to call right when the IRS opens eastern time or late in the day before closing.

Does the IRS owe you interest on late refunds?

Even with the delays, the IRS owes you interest on your money. The IRS has administrative time (typically 45 days) to issue your refund without paying interest on it.

You have until April 18 to file your taxes for this year. If you don’t receive a refund within 45 days after the deadline, then interest may be owed by Uncle Sam.

What Makes a Business Sustainable?

When we are talking about building a sustainable business, we are talking about one that is built to last.

Often, entrepreneurs get caught up in the headlines about businesses with hyper-growth rates. We start thinking of how we can replicate these results.

But what is often missing is these results are just short-term, fueled by outside money or poor business models that are not sustainable.

There are many examples of the crash and burn businesses that are all the rage but come crashing down. WeWork comes to mind as a perfect example.

Understanding how to build a sustainable business might be the difference between success and failure.

Here are some tips to building a business meant to last:

1) Be nimble

We have all read about the crash and burn start-ups or the established businesses that suddenly can’t compete and are stuck on life support (Ex: Blockbuster, Sears, Blackberry). Big companies, by their nature, are not agile. They get stuck in bureaucracies and fear of risks that let smaller upstarts outflank them.

2) Listen to your customers

The pandemic showed us that human decisions and economic trends could be flipped in a very short period of time. From the great resignation to remote work, consumers have changed their behavior. Entrepreneurs need to listen to their customers to develop personas and segments to understand their unique pain points and needs better.

Ask for customer feedback.

Start customer advisory boards.

Track your critical KPIs.

From this data, you can be quick enough to take advantage of consumer trends and pivot your offering to meet these new realities.

3) Listen to your employees

The pandemic has caused a shift in the workforce. Listen to your employees to share their needs and aspirations with you, as this will help them feel supported by the company during these difficult times. Keeping an employee’s unique perspective becomes necessary for the survival or success of business operations due to changing conditions like increased competition from other companies who are also listening closely because it pays off big time! Help out those workers trying hard but stretched thin–it is important both physically AND mentally before anything else begins.

4) Budget, budget, budget

If anything, the pandemic has taught us that revenue streams can dry up overnight. From supply chain delays, government regulations to inflation pressures, your margins are threatened more than ever.

It is difficult to know when your business will be profitable and what resources you might need without a proper budget. It can also make operating within one’s means more challenging as unexpected costs arise from the unpredictable nature of life (elements such as illness).

A detailed analysis that includes all probable expenses helps identify available capital for future growth opportunities while estimating how many dollars should go towards fixed or variable cost components to achieve maximum returns on investment.

A well-thought-out financial plan provides clarity around these topics: predicting revenue streams, deciding which type(s)of assets best fit company needs, and whether debt or equity financing is required.

5) Own a brand position

Too many businesses try to be all things to all companies. But the most successful brands are very targeted in their message, market, and the problem they are trying to solve. Sometimes it takes a leap of faith to focus on a smaller audience. But positioning your business is the fastest way to grow and utilize pricing power.

6) Retain your key employees

High employee turnover is a significant headwind to business sustainability. If you are constantly replacing key team members, you delay success in lost hours in training. These lost opportunity costs will make it harder to build a sustainable business. Investing in your key managers makes the life of the entrepreneur easier.

Internal training, streamlined processes, and improving efficiency are the key to scalability. This will allow you more time for external growth while still achieving results.

7) Be authentic

Many big corporations and entrepreneurs act more like chameleons, changing their belief systems based on the audience or the timing of the day. You are a leader when you lead with your heart and not just for the sake of it. Your true colors show in how others perceive you, so be authentic. Your employees and your customers will see this passion and follow it. Foster an environment that’s infused with curiosity by rewarding those who go against traditional norms or follow their passions – because we all need more inspiration now than ever before.

8) Partner wisely

This is true from every relationship you get into in business. By your choice of co-founders, investors, outsourced teams, and vendors (ex: your accounting firm), your decisions will impact your odds for success.

Always surround yourself with those that will make you better.

Closing

A sustainable business has fewer bumps in the road, from buying out a disgruntled founder to an investor with timelines that don’t match yours or the market. Closing A sustainable business is one where profitability and growth rates are in harmony. Running a sustainable business involves using your resources economically, where cash flow and budgeting lead to long-term success. Sacrificing the future for a short-term expansion may not always be the best strategy.

We partner with aspiring entrepreneurs to put them on the path to sustainability. Feel free to reach out to see how we can help you achieve your dreams.

Important Enhancements to the Earned Income Tax Credit For 2021

The earned income tax credit (EITC) is regarded as one of the government’s largest antipoverty programs and helps millions of American families every year. You are urged to check to see if you qualify for this very beneficial refundable credit. Significant enhancements have been added (some only for 2021), and even if you have not qualified in the past, you may qualify this year.

If you are not normally required to file a tax return because your income is below the filing threshold, you could qualify for this credit. You may also qualify for the child tax and the recovery rebate credits, plus get a refund of any income tax withholding you had during 2021, so don’t assume there is no benefit from filing a tax return.

The IRS estimates that one in five individuals eligible for EITC fail to claim it simply because they don’t understand the criteria. Plus, many individuals who never qualified for the EITC previously may be eligible in 2021 because their income will be lower because of the COVID pandemic. Nationwide last year, almost 25 million eligible workers and families received over $60 billion in EITC with an average EITC of $2,411.

To qualify for the EITC you must have earned income. Earned income is generally income from working, such as wages and net self-employment income, but also includes tips, union strike benefits, nontaxable military combat pay and nontaxable parsonage allowances for clergy. Wages for this purpose includes wages before reductions due to salary deferrals such as 401(k)s, cafeteria plans, and excludable dependent care benefits.

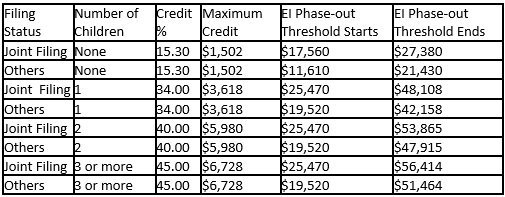

There are several changes to EITC for 2021 that will allow significantly more individuals to qualify for the credit. Generally, the age threshold to claim the EITC is 19, with certain exceptions, and with no upper cap on age. In the past, the EITC was only available to people ages 25 to 64. In addition, individuals may have investment income of $10,000 (up from $3,650 in 2020) and still qualify for EITC. Childless workers and couples can qualify for the EITC if their earned income is below $21,430 ($27,380 for joint filers), and the maximum credit for a taxpayer with no qualifying children is $1,502, up from $538 in 2020.

As mentioned previously, the EITC is based on the amount of your earned income and whether there are qualifying children in your household. The credit increases as the taxpayer’s earned income or adjusted gross income (AGI) increases, until it reaches a plateau, where it remains constant at the maximum credit amount until it reaches the AGI phase-out threshold. Once the threshold amount is exceeded, the credit is reduced by a set percentage, and no credit is allowed once the income exceeds the top of the phase-out range. The following table illustrates the maximum credit and phase-out ranges based on filing status and number of children for 2021.

Qualifying children – A qualifying child must be under the age of 19 or be a full-time student under age 24 at the end of the tax year. This age test does not apply to a child who is permanently and totally disabled. In addition, they must meet relationship and residency tests.

2019 AGI – There is a special rule for 2021 only: Where a taxpayer’s 2021 earned income is less than their 2019 earned income, the taxpayer can elect to use the 2019 earned income amount to compute the 2021 EITC. This was put into effect for taxpayers whose income has decreased because of COVID but applies to anyone who chooses to use the 2019 AGI. However, one must be cautious when making the choice to ensure the AGI that produces the best result is used.

Selecting the 2019 AGI to compute the EITC will have no effect on the 2021 income tax since the 2021 AGI will be used for that computation. Taxpayers should also note that any Economic Impact Payments or Child Tax Credit payments received are not taxable or counted as income for purposes of claiming the EITC. Eligible individuals who did not receive the full amount of their Economic Impact Payment may claim the Recovery Rebate Credit on their 2021 tax return.

Separated Spouses – Married but separated spouses can choose to be treated as not married for EITC purposes. To qualify, the spouse claiming the credit cannot file jointly with the other spouse, must have a qualifying child living with them for more than half the year and either:

- Not have the same principal residence as the other spouse for at least the last six months out of the year, or

- Be legally separated according to their state law under a written separation agreement or a decree of separate maintenance and not live in the same household as their spouse at the end of the tax year for which the EITC is being claimed.

Child Does Not Have an SSN – Single people and couples with children who do not have Social Security numbers cannot claim the EITC available for taxpayers with children. But they can claim the smaller EITC available to childless workers. In the past, these filers didn’t qualify for any credit.

Refunds Delayed – Because of substantial fraud related to refundable credits, Congress revised the tax law a few years ago so that the IRS cannot issue refunds before mid-February for tax returns that claim the EITC or the Additional Child Tax Credit (ACTC). The IRS must hold the entire refund, giving the agency more time to detect and prevent errors and fraud.

Active Military – Members of the military can elect to include their nontaxable combat pay in their earned income for the earned income credit. If that election is made, the military member must include all nontaxable combat pay received as earned income. If spouses filing a joint return both received nontaxable combat pay, then each one can make a separate election. Disabled Individuals – Disabled individuals frequently overlook the opportunity to claim EITC. Even though they may not be working and earning income, certain disability income is treated as earned income for purposes of the EITC and includes the following amounts:

- Disability benefits attributable to the employer’s payment of disability policy premiums. However, nontaxable disability income from policies whose premiums the employee paid, and Social Security benefits, are not “earned income” for purposes of the EITC.

- Long-term disability benefits to an individual who is retired on disability are only earned income until the individual reaches the minimum retirement age, which is generally the earliest age at which the individual could receive a pension or annuity if not disabled.

If you qualify for but failed to claim the credit on your return for 2018, 2019 and/or 2020, you can still claim it for those years by filing an amended return or an original return if you have not previously filed.

If you have questions about your qualifications for this credit or need help amending or filing a prior year’s return to claim the credit, please give our office a call.

5 Tax Planning Tips For Retirees

There’s a common misconception that, when you retire, your tax bills shrink, your tax returns become simpler and tax planning is a thing of the past. That may be true for some, but many people find that the combination of Social Security, pensions and withdrawals from retirement accounts increases their income in retirement and may even push them into a higher tax bracket.

If you’re retired or approaching retirement, consider these five tax-planning tips:

1. Take inventory. Estimate how much money you’ll need in retirement for living expenses and inventory your income sources. These sources may include taxable assets, such as mutual funds and brokerage accounts; tax-deferred assets, such as IRAs, 401(k) plan accounts and pensions; and nontaxable assets, such as Roth IRAs, Roth 401(k) plans or tax-exempt municipal bonds. Social Security benefits may be nontaxable or partially taxable, depending on your other sources of income.

Develop a plan for drawing retirement income in a tax-efficient manner, being sure to keep state income tax, if applicable, in mind. For example, you might minimize current taxes by tapping nontaxable assets first, followed by assets that generate capital gains, and putting off withdrawals from tax-deferred accounts as long as possible.

On the other hand, if you’re approaching age 72 and will have substantial required minimum distributions (RMDs) from tax-deferred accounts when you reach that age (see No. 3 below), it may make sense to withdraw some of those funds earlier. Why? It can help you avoid having large RMDs that would push you into a higher tax bracket later.

For example, you might withdraw as much as you can from IRAs or 401(k) accounts each year without exceeding the lower tax brackets. That way, you keep current taxes on those funds at a reasonable level while reducing the size of your accounts and, in turn, the size of your RMDs down the road. You can obtain additional funds from nontaxable or capital gains assets, if needed.

2. Consider the timing of Social Security benefits. You can begin receiving Social Security benefits as early as age 62 or as late as age 70. The later you start, the larger the benefit amount — so, if you don’t need the money right away, putting it off may be a good investment. Also, benefits are reduced if you start them before you reach full retirement age and continue to work.

Keep in mind that, if your income from other sources exceeds certain thresholds, your Social Security benefits will become partially taxable. For example, married couples filing jointly with combined income over $44,000 are taxed on up to 85% of their Social Security benefits. (Combined income is adjusted gross income plus nontaxable interest plus half of Social Security benefits.)

3. Make qualified charitable distributions. You’re required to begin RMDs from tax-deferred retirement accounts once you reach age 72 (up from 70½ for people born before July1, 1949) though you’re able to defer your first distribution until April 1 of the year following the year you reach age 72. RMDs generally are taxed as ordinary income and you must take them regardless of whether you need the money. As noted in No. 1, a large RMD can push you into a higher tax bracket.

One strategy for reducing the amount of RMDs, at least if you’re charitably inclined, is to make a qualified charitable distribution (QCD). If you’re age 70½ or older (this age didn’t increase when the RMD age increased), a QCD allows you to distribute up to $100,000 tax-free directly from an IRA to a qualified charity and to apply that amount toward your RMDs.

The funds aren’t included in your income, so you avoid tax on the entire amount, regardless of whether you itemize. In addition, the income-based limits on charitable deductions don’t apply. Any amount excluded from your income by virtue of the QCD is similarly excluded from being treated as a charitable deduction.

4. Pay estimated taxes. Your retirement income sources may or may not withhold income taxes. To avoid tax surprises and penalties, estimate whether your withholdings will be sufficient to pay your tax liability for the year and make quarterly estimated tax payments to cover any expected shortfall.

5. Track your medical expenses. Currently, medical expenses are deductible only if you itemize and only to the extent they exceed 7.5% of your adjusted gross income. If you have significant medical expenses, track them carefully. Then if you exceed this threshold or are close to exceeding it, consider bunching elective expenses into the year to maximize potential deductions.

If you’re nearing retirement age and have questions on how your tax situation may change, contact your tax advisor.

© 2021

5 Affordable Ways to Share the Holiday Spirit

The holidays are a season of giving. While much of this involves financial expenditures, you can also give in ways that are more affordable and may hold more meaning. Here are some suggestions about how you can engage in acts of generosity and return to what the season is all about.

Cook Food

Nothing nourishes the heart and soul, not to mention your stomach, like food made with love from your own kitchen. Baking cookies is always an easy and fun thing to do, but a main dish (with protein) or hearty casseroles are also good options. People who are homebound due to an illness, those going through financial difficulties, or even new moms will appreciate the gift of a warm meal. You might also ask co-workers, local churches, or homeless shelters if they’re looking for some extra sustenance during this time of year.

Create Necessity Bags

Giving to the unhomed during the holidays is an easy, inexpensive way to make a difference. Fill a gallon-sized food storage bag with things like gloves, toothpaste and toothbrush, hand sanitizer, sanitary wipes, bottled water, snacks, and a gift card to a grocery store. Then contact your local organizations and charities to see where the needs lie. You might also carry these bags in your car and when you see someone, give one to them. Moments like these are invaluable to those in need and for you, too.

Volunteer Time

Showing up with an extra pair of hands is often what someone needs. A great place to check out is VolunteerMatch. Just type in your ZIP code and you’ll find all kinds of opportunities to help everyone from seniors to children in many sectors, including education, arts, and health. You might also find ways to help animals or read to the blind. These are feel-good, money-free ways to experience the joy of giving.

Donate Craft Items

How many times have you thrown away your toilet paper rolls or egg cartons? This year, save and donate them to nearby schools or community centers. All it takes is a few phone calls to find out what their craft needs are. You’ll also be helping the environment – sharing some love for Mother Nature. How simple is that?

Declutter Your Dwelling

This one has so many terrific benefits. You can get rid of clothes and belongings that crowd your closets, which is a wonderful feeling. One option is to sell them on eBay Charity and donate to a nonprofit of your choice. You choose what percentage of the sale goes to the organization (from 10 to 100 percent). eBay will even give you a credit on your selling fees based on the percentage you choose. If you want to give away gently used professional clothes, Dress for Success and Jails to Jobs, are groups that empower people to look their best when making a fresh start. If you’d like to rid yourself of shoes you’ll never wear again, Soles4Souls is a great resource and you can ship up to 15 pairs of shoes without paying a fee through the Zappos for Good program. Talk about good for the sole, er, soul!

For the most part, should you choose to get into the holiday spirit with these activities (aside from a few costs here and there), the main thing you’ll be spending is time. However, experiencing the joy of giving is priceless.

Sources

How Businesses Can Recognize and Combat Employee Burnout

According to the job site Indeed, COVID-19 has taken a toll on workers even more in 2021, compared to 2020. The survey conducted by Indeed found that 52 percent of those surveyed felt “burned out” in 2021. Sixty-seven percent of those asked said that feeling burned out has become more pronounced as COVID-19 has progressed. It’s more noticeable among remote workers (38 percent), compared to 28 percent of employees working in person.

Gallup reported in October 2020 that between 2016 and 2019, worker burnout was already on the radar. Once COVID-19 hit workers in 2020, those working remotely 100 percent of the time were reporting even higher levels than those who work outside the home.

Pre-COVID-19, when employees worked remotely either 100 percent of the time or via a hybrid approach, they had lower levels of burnout compared to those who worked at their place of employment full-time.

When it comes to remote-only employees who “experience burnout at work always or very often,” levels have gone from 18 percent pre-pandemic to 29 percent during the coronavirus pandemic.

This phenomenon is blamed on not being able to choose to work remotely or at the workplace – the choice is not there with COVID-19. As of September 2020, 4 in 10 full-time employees worked exclusively from home, compared to 4 out of 100 pre-COVID.

According to the Mayo Clinic, “job burnout is a special type of work-related stress.” Internal factors, according to the Mayo Clinic and Gallup, include uneven treatment by management, excessive work assigned to an individual, a toxic workplace, and ambiguous or unclear assignment instructions.

Outside factors such as their personal life, their natural disposition, mood disorders, etc. may add to it. When a worker is fatigued, physically or intellectually, this also grips the worker with a feeling of lower productivity and a loss of who they are professionally.

For those who can’t manage job-related stressors, burnout often leads to negative results. According to the Centers for Disease Control and Prevention (CDC), this includes feeling dubious about one’s future at the company, experiencing an inability to sleep, experiencing an inability to concentrate, feeling tired, and having little motivation to complete one’s work.

For employees facing a completely new way of working, the unpredictability of being exposed to COVID-19, having to juggle work and personal obligations throughout the workday, and the inability to access the right tools to get work tasks completed, burnout will likely ensue.

Managing Burnout

There are many recommendations to regain control and keep work-related stress in check. They include creating a schedule for both regular sleep and time to fulfill work tasks, if feasible. Taking strategic breaks and finding constructive non-work interests can lessen the stress of work as part of a balanced schedule.

According to Gallup, managers must harmonize maintaining high-performance expectations with employee commitment to the organization and worker welfare.

Gallup credits effective managers and “organizational communication” with keeping full-time remote workers fully engaged by making them feel like an integral part of their company. Through purposeful training and crystal-clear expectations, workers are set up for success.

The CDC offers recommendations for how workers can reduce the effects of burnout. Staying diligent with emotional wellbeing treatments and recognizing and getting treatment for new substance abuse issues is recommended. Staying in touch with others can help both sides feel supported mentally and lower stress. Taking a break from constant negative news is also recommended.

Much like businesses, employees are unique. With COVID-19 impacting each of us differently, managers must evaluate their organization’s circumstances and employees to find a balance between employee performance and their ability to maintain wellbeing.

Sources

https://www.cdc.gov/coronavirus/2019-ncov/community/mental-health-non-healthcare.html

https://www.gallup.com/workplace/323228/remote-workers-facing-high-burnout-turn-around.aspx

https://www.mayoclinic.org/healthy-lifestyle/adult-health/in-depth/burnout/art-20046642

https://www.indeed.com/lead/preventing-employee-burnout-report

Tax Benefits When Saving for College Education

A common question among parents is, “How might I save for a child’s post-secondary education in a tax beneficial way?” The answer depends on how much the education is expected to cost and how much time is left until the child heads off to college or a university or enters an apprenticeship program.

The amount of funds that will be required will depend upon whether your child will be attending a local college, attending a local college and then transferring into a university, going straight to a university, or beginning an apprentice program. If the child will be attending college or an apprenticeship locally, you generally only need to be concerned about tuition, books, and other class materials, and the child can live at home, whereas the child attending a university, unless it is local, will add housing and food costs on top of substantially higher university tuition. Another factor is whether the student will leave school after obtaining a bachelor’s degree or will be doing graduate studies for an advanced degree.

When the time comes, your child may qualify for a scholarship or grant, but you can’t depend on that when working out a college savings plan.

The federal tax code has two beneficial savings plans to use. Neither plan provides a tax benefit to making the original contributions. The benefit is that growth due to appreciation of the investments, if any, and earnings (dividends and interest) are tax-free when withdrawn for qualified education expenses. Thus, the sooner each plan is started, the better, because it will have more years to grow in value.

Both savings plans allow the funds to be used for kindergarten education and above. However, these plans provide tax-free accumulation, and the more the funds are used for expenses at lower levels of education, the less tax benefits they will provide. Careful consideration should be given to using these savings plans for anything other than post-secondary education.

More tax benefits will be gained by front-loading the contributions and thus having a larger amount for which the growth and earnings can be compounded. You should also be aware that anyone, not just you, can make a contribution to the child’s college savings plans. So if your child has any well-heeled grandparents, other relatives, or friends who would like to help, they can also contribute.

The two savings plans currently available for college savings are the Coverdell Education Savings Account and the Qualified Tuition Plan, most commonly referred to as a Sec. 529 plan (529 denotes the section of the tax code that governs it).

Coverdell Education Savings Account – This type of plan only allows up to $2,000 in contributions per year, which generally rules it out as a practical method for college savings, other than as a supplement to other means of saving.

Sec. 529 Plan – This approach is likely your best option. State-run Sec. 529 plans allow significantly larger amounts to be contributed; multiple people can each contribute up to the gift tax limit each year without being subjected to gift tax reporting. This limit is $15,000 for 2021, and it is periodically adjusted for inflation; in 2022, it will increase to $16,000. A special rule allows contributors to make up to five years of contributions in advance (for a total of $75,000 in 2021 and $80,000 in 2022).

Sec. 529 plans allow taxpayers to put away larger amounts of money, limited only by the contributor’s gift tax concerns and the intended plan’s contribution limits. There are no limits on the number of contributors and no income or age limitations. The maximum amount that can be contributed per beneficiary (the intended student) is based on the projected cost of college education and will vary among the states’ plans. Some states base their maximum on an in-state four-year education, but others use the cost of the most expensive schools in the U.S., including graduate studies. Most have limits over $200,000, with some topping $530,000. Generally, additional contributions cannot be made once an account reaches that level, but this doesn’t prevent the account from continuing to grow.

Taxpayers are not limited to participating in the 529 plan offered by their state of residence and can shop around for the plan with the best growth potential and highest maximum contribution.

When the time comes for college, the distributions will be part earnings/growth in value and part contributions. The contribution part is never taxable, and the earnings part is tax-free if used to pay for qualified college expenses. In addition, the portion of the distribution representing the return on the contributions, if used for qualified education expenses, will qualify for the American Opportunity Tax Credit, which can be as much as $2,500, provided your income level does not phase it out.

Gifts – In addition to the annual gift tax exclusion, a donor may make gifts (with no specific dollar limitation), which are totally excluded from the gift tax when making payments directly to an educational institution for tuition. This includes both college and private primary education. However, these gifts can only pay for tuition, which does not include books, supplies, or room and board. It is critical that the payments be made directly to the educational institution for them to be excluded from the gift tax. Reimbursement paid to the donee will not qualify.

The tuition exclusion is often overlooked yet can be beneficial. For instance, a grandparent can use the tuition gift to reduce their estate while helping a grandchild pay for tuition and giving the child’s parents an education credit at the same time.

For additional details or assistance in planning for a child’s higher education, please give our office a call.