Categories for

Small Businesses: Here’s How the U.S. Supreme Court Wayfair Decision Affects You

If you are a small business owner, chances are good you’re paying more attention to your accounts receivables and deliverables than to a three-year-old Supreme Court decision. But knowing what happened in the Wayfair decision on June 21st of 2018 is important if you do a significant amount of business in states other than where you have a physical presence.

The Wayfair decision reversed the earlier “Quill” decision made back in 1992, and in doing so it forever changed the tax liabilities of businesses. The Quill case established that businesses were not required to collect or remit sales or sellers use taxes for states in which they lacked a substantial physical presence. But the “burdensome” administrative processes that were eliminated with that decision became the law of the land with the Wayfair decision, which established economic nexus for the state of South Dakota as either 200 transactions shipped to state residents or companies per year, or $100,000. Once that threshold is reached, states can require out-of-state companies to collect and remit sales and use taxes from their customers.

Compliance with these requirements is no small thing, and the earlier court decision was correct in referring to it as “burdensome.” But failing to comply has very real consequences in the form of back taxes and penalties. The solution is automation, almost by necessity: Without that kind of help, organizations would need at least one employee dedicated to nothing but managing and tracking sales volumes for each state as well as the various local and state regulations.

To get an idea of exactly how complex the tax could be, consider this: There are approximately 10,000 different tax jurisdictions in the United States, and identifying all of them goes beyond anything as simple as zip code, county, or city borders. Though it would be nice to think that everybody adhered to standard taxability rules as is the case for SST member states, the fact is that each jurisdiction can have its own rules regarding what does and does not get taxed. Not only does this apply to product categories like clothing, food, or luxury items, but also to services such as shipping and handling or product usage. Each rule needs to be identified and adhered to, or risk fines and penalties.

In addition to learning the rules and tax thresholds for nexus for each state, compliance requires adhering to the process that each state imposes. These are usually coordinated via state tax portals, meaning that sellers will need to have this information easily at hand – for as many as 50 states. And sellers will be responsible for tracking when tax requirements change, for every jurisdiction.

Though some states offer resale exemption certificates, following the processes required to administer those certificates has turned out to be a bridge too far for many companies. Much of this is due to the fact that – as is true with other aspects of compliance – the certificates and rules for certificate renewals have to be collected and learned for each state and is an additional burden. But failure to properly fill the certificates out can lead to them being taxed on that revenue, and lead to penalties and interest being imposed if those taxes are not properly collected.

Though following the rules represents an enormous headache and the need to invest time and money, doing so is preferable to being audited and penalized. By creating a strategy for dealing with these rules, you can not only eliminate your risk of non-compliance but also have a plan in place in case you do receive an audit letter. We strongly encourage you to contact us as soon as you receive an audit letter and do so before providing any response or submitting any information to a regional tax agency. We will be able to provide you with the information you need about how to best manage the situation.

Mid-Year Tax Planning Checklist

All too often, taxpayers wait until after the close of the tax year to worry about their taxes and miss opportunities that could reduce their tax liability or financially assist them. Mid-year is the perfect time for tax planning. The following are some events that can affect your tax return; you may need to take steps to mitigate their impact and avoid unpleasant surprises after it is too late to address them. Here are some events that can trigger tax consequences. Did you (or are you going to):

- Get married, divorced, or become widowed?

- Change jobs or has your spouse started working?

- Have a substantial increase or decrease in income?

- Have a substantial gain from the sale of stocks or bonds?

- Buy or sell a rental?

- Start, acquire, or sell a business?

- Buy or sell a home?

- Retire this year?

- Reach age 72 this year?

- Refinance your home or take out a second home mortgage this year?

- Receive a substantial inheritance this year?

- Take advantage of tax-beneficial retirement savings?

- Make any significant equipment purchases for your business?

- Purchase a new business vehicle and dispose of the old one?

- Adequately document your cash and non-cash charitable contributions?

- Keep up with your self-employed estimated tax payments?

- Make any unplanned withdrawals from an IRA or pension plan?

- Add a solar electric system to your home or purchase an electric vehicle?

- Hire veterans’ or other individuals in your business that may qualify for the work opportunity tax credit?

- Trade in cryptocurrency?

- Defer employer payroll taxes in 2020?

- Incur expenses adopting a child?

- Start receiving Social Security benefits?

- Exercise an employee stock option?

- Start using a part of your home for business this year?

- Exchange real properties used in your trade or business or held for investment?

- Start a retirement plan in your self-employment business?

- Make gifts of over $15,000 to anyone individual this year?

- Receive advance child tax credit payments?

Of course, these are not the only issues that have tax consequences.

If you anticipate or have already encountered any of the above events or conditions, it may be appropriate to consult with our office—preferably before the event—and definitely before the end of the year.

How to Catch Up on Your Retirement

If you’re 40 or 50 and aren’t where you’d like to be in terms of saving for retirement, don’t despair. You can remedy this situation. And since people are living well into their 80s and 90s, it’s never too late to start. Here are a few things you can do.

Max Out Your 401(k)

This could be a game-changer. Stuart Ritter, a certified financial planner with T. Rowe Price, recommends that you save at least 15 percent of your income for retirement, including the amount your employer matches. If your company is contributing 3 percent, then you should save 12 percent. If you can’t go this high, then increase the amount by 2 percent each year. So, if you’re saving 3 percent this year, bump it up to 5 percent, then 7 percent, and so on. If you’re under 50, try to hit the $19,500 limit. After you turn 50, you can increase your annual savings to $6,500 on top of this $19,500 limit. Note: You have to be 59 ½ to withdraw money without any penalties. However, the early withdrawal penalty doesn’t apply if you’re 55 or older in the year you leave your employer. All this to say that the sooner you start doing this, the more you will save and the more you’ll have down the road.

Contribute to a Roth IRA

With this product, you can grow your money on a tax-deferred basis. For instance, if you’re 40 and invest $6,000 each year at an 8 percent return, then by the time you’re 65 you’ll have more than $473,726. Even if you wait until you’re 50 and save 6k a year, using the same rate of return, you’ll save as much as $175,946 by the time you’re 65. However, there are some income limitations. If you’re single and your modified adjusted gross income is more than $125,000, your contribution limit is reduced. If you’re single and make over $140k, you can’t contribute. Michelle Buonincontri, a certified financial planner, says that the beauty of Roth IRAs is that they allow for tax-free compounding. Further, when withdrawal rules are followed, the withdrawals, including the earnings, will be tax-free. And when you’re in the withdrawal phase, it can minimize taxable income, which can add up and help your money last longer during retirement.

Take Advantage of Your Deductions

Not everyone takes standard deductions. That’s why if you have a significant amount of mortgage interest, deductible taxes, charitable donations, and business-related expenses that your employer doesn’t reimburse you for, you’ll most likely want to itemize your deductions. Talk to your CPA and figure out whether this is a good plan for you. Then, start saving your receipts and keeping good records. As you get closer to retirement and if money is tight, remember: it’s not what you make, but what you save that makes the difference.

Don’t Forget About Home Equity

While home equity probably shouldn’t be used as your main source of income when you’re retired, it’s a viable solution. Retirees might consider borrowing against it to fund living expenses. In fact, you can use a home equity line (HELOC) to draw from when needed. Other options include selling, downsizing, and either living off the equity or investing it. But before you sell, you should consider tax consequences. Married homeowners who file a joint tax return can make up to $500k without owing taxes on capital gains. If you’re single, the cap is $250,000.

Get Disability Coverage

The reason for this is simple: to protect yourself and at least a portion of your income and retirement savings in a worst-case scenario. It is always a good idea to have a contingency plan.

Consider Your Cash Value Policies

This is the last resort, but again, a good option, especially if the original need for your insurance policy is no longer there. However, before you do anything or access its cash value, consult your tax advisor or insurance professional first.

No matter what your situation is, you can save for your future. All you have to do is begin now and take it one day at a time.

Sources

https://www.investopedia.com/articles/retirement/08/catch-up.asp

https://www.kiplinger.com/retirement/retirement-planning/602191/401k-contribution-limits-for-2021

How and Why to Develop a Bring-Your-Own-Device Policy

With the internet available for essentially all employees and remote work becoming a part of more businesses’ operations, developing a bring-your-own-device (BYOD) policy is almost necessary to help employees be more productive and safe while working. Research shows there are many reasons why businesses should develop the right type of BYOD policy.

According to Intel and Dell, 61 percent of Gen Y and 50 percent of workers 30 and older think the electronic devices they use at home are more capable of completing tasks in their everyday life compared to their work devices.

Frost & Sullivan found that connected handheld technology helps employees, making them about one-third more productive and reducing their average workday by 58 minutes.

A BYOD policy simply means that companies permit their workers to use their own smart devices to perform job-related tasks. It can be beneficial for a company, especially a smaller one; however, it’s important to evaluate the advantages and disadvantages before implementing this type of policy.

Advantages

One of the most obvious reasons for a business to develop and implement a BYOD policy is due to the proliferation of technology. Along with saving employers money by not having to provide a work device, there is no need to provide costly training on how to use the device. A 2016 Pew Research survey determined that 77 percent of U.S. adults have a smartphone. For those ages 18 to 29, more than 9 in 10 (92 percent) own a smartphone. In 2021, even more adults likely have at least one smartphone.

Potential Drawbacks/Legal Considerations

According to a 2017 Pew Research Center report, there’s a significant portion of smartphone users with less-than-ideal security habits. For example, 28 percent of respondents don’t secure their phone with a screen lock or similar features. Forty percent said they update their apps or phone’s operating system only when it’s convenient for them. Less common, but equally alarming: Between 10 percent and 14 percent of respondents never update their phone’s operating system or apps.

Without a proper system set up, there are more security risks, including reduced or compromised company privacy and a lack of basic digital literacy among employees. Mobile Device Management software can help monitor, secure, and partition personal and business files in a dedicated area, providing more confidence when permitting employees to BYOD.

Other considerations for a BYOD policy include prohibiting employees from downloading unauthorized apps; performing local back-ups of company data; disallowing syncing to other personal devices; not allowing modifications to hardware/software beyond routine installations; and not using unsecured internet networks.

Depending on how employees are classified by the Fair Labor Standards Act (FLSA) for overtime compensation, businesses may be liable for overtime wages if non-exempt employees perform their duties outside the office. If non-exempt employees perform duties beyond “40 hours of work in a workweek,” as the U.S. Department of Labor outlines, businesses could be liable for additional wages paid if they use their device for work-related tasks.

While each company has its own needs and unique workforce, crafting a BYOD policy that increases productivity while maintaining security and privacy can give businesses a competitive edge.

Sources

https://www.pewresearch.org/fact-tank/2017/01/12/evolution-of-technology/

What is a Net Zero Economy?

President Biden re-entered the United States in the Paris Agreement. This is an international treaty first signed in 2015 in which countries around the globe committed to mitigating climate change. Specifically, the goal of the Paris Accord is to limit global warming to no more than 1.5 degrees Celsius above pre-industrial levels.

This objective would generate what is called a net-zero global economy, which means creating a balance between the amount of greenhouse gases produced and the amount of greenhouse gasses removed from the atmosphere. The main engine that places carbon back into the soil is healthy vegetation that grows year-round, called cover crops and reforestation.

The initial benchmark is to achieve net-zero carbon dioxide emissions by 2050 and net-zero emissions of all greenhouse gases by 2070. However, accomplishing these lofty goals will require a remarkable transformation of the global economy and global farming practices.

A way to measure global warming is through “temperature alignment” — a forward-looking benchmark that compares the level of emissions today against the potential for reducing them by a certain date in the future. The measure can be applied to a specific business, government, or investment portfolio.

For investors, global greening provides an opportunity to invest in companies positioning for a future net-zero economy. After all, it’s important to recognize that climate risk represents substantial investment risk. Companies that prepare for the transition to sustainable energy sources will be able to deliver long-term returns, while those that do not could become obsolete.

If Net Zero is your path, consider the following steps to align your investment allocation with the goals of a net-zero economy. For example:

- Reduce your exposure to high-carbon emitters and companies not making forward-looking commitments to transform to the net-zero economy.

- Prioritize investment decisions based on companies actively reducing reliance on fossil fuels and meeting science-based targets.

- Target specific sustainable sectors (e.g., clean energy, green bonds) based on your asset allocation strategy – and diversify investments among those holdings.

- Monitor ongoing research and available data to measure temperature alignment to ensure your issuers and investments are meeting published transition plans. This benchmark should be reviewed with the same rigor as traditional financial data.

The United States and the entire world have a choice to reduce global carbon emissions. However, the effort also offers an opportunity to invest in climate innovation. The future will bring the survival of the fittest, is your portfolio ready.

Customers Paying Late? How to Create Statements

After the year-plus you’ve just experienced, the last thing your small business needs is customers who are behind on their payments to you. You may have been giving them a break because you know that they’re struggling, too, but things have been looking up for many companies in the past few months. It’s time for you to be more proactive about calling in your debts.

There are numerous ways you can accomplish this. One of the best is to send statements in QuickBooks Online, which are detailed reminder forms that contain multiple transactions. These can be especially helpful if you’ve sent multiple invoices with no response. There are three different types you can send, depending on your needs. Here’s how you create them.

Before You Start

QuickBooks Online offers a couple of options for formatting your statements. To see these, click the gear icon in the upper right corner and select Your Company | Account and Settings. Click the Sales tab and scroll down to the Statements section. Click the pencil icon over to the far right to make any changes needed. You can:

- List each transaction as a single line or include all of the detail lines.

- Display an aging table at the bottom of each statement.

Click the buttons to specify your preference and then click Save and Done.

QuickBooks Online gives you control over some elements of your statements.

Three Statement Types

You can choose from among three different types of statements in QuickBooks Online: Balance Forward includes invoices with outstanding balances for a specified range of dates. Open Item statements contain information about all unpaid (open) invoices from the last 365 days. And Transaction Statements show every transaction in a date range that you specify. We’ll describe how to create them so you can decide which makes the most sense for a particular situation.

One Way to Create Statements

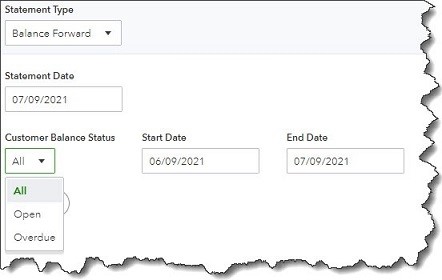

Like it does for many other actions, QuickBooks Online offers two ways to create statements. The first is easier. Click the New button in the upper left and select Statement (under Other). Click the down arrow in the field under Statement Type to see the three options there.

If you select Balance Forward, you’ll need to define three criteria (there will be similar options for the other two types):

- Statement Date

- Customer Balance Status (Open, Overdue, or All)

- Start Date and End Date

QuickBooks Online makes it easy to create any of three types of customer statements.

When you’re satisfied with your statement parameters, click Apply. QuickBooks Online will display a list of the transactions that meet your criteria, along with the number of them that will be generated. Each row in the list will display the recipient’s name, email address, and balance. In the upper right corner, you’ll see the number of statements again and the total balance these customers represent.

If you want to exclude any of these customers, click in the box in front of each to unselect them and delete the checkmark. When you’re satisfied with your list, click Save, Save and send, or Save and close. If you click Save and send, a window will open containing a preview of your statements. Thumbnails of each will appear in the left pane. Click on any to see their previews. When you’re ready, you can download, print, or send them.

If you click Save or Save and close, you’ll still be able to see the statements you’ve just generated. Click the Sales tab in the toolbar, then All Sales. Click the down arrow next to Filter and open the drop-down list under Type. Select Statements, and your list will appear. You can print or send one by selecting the correct option in the Action column. If you want to dispatch multiple statements, click in the box in front of each, and then click the down arrow next to Batch actions.

Another Method

There’s an alternate way to create statements. Click the Sales tab in the toolbar, then Customers. Select any or all of the customers in the list, then click the down arrow next to Batch actions and select Create statements. QuickBooks Online will open the Create Statements window again so you can select the type and process your statements like you did using the previous method.

We don’t expect that you’ll have much trouble working with statements, though you may want to consult with us on when they’re appropriate. We can also suggest other ways to bring your accounts receivable up to date. As always, we’re available to help you maximize and streamline your use of QuickBooks Online. Keeping your financial books current and organized is one way to ensure that you don’t fall too far behind with customer payments.

Entrepreneur Success Story: How Canva Reached a $15 Billion Evaluation and Made Its Young Founders Billionaires

Human beings are visual learners – they always have been, and they always will be.

A big part of this has to do with the way that the human brain works. According to one recent study, when people hear information, they generally only remember about 10% of what they’re exposed to. If that information is paired with relevant visuals – be it in the form of a video or even static content like a photo or infographic – they remember 65% of it on average. All told, it’s estimated that between 51% and 80% of all businesses in every industry will rely heavily on visual content in 2021 – a trend that shows absolutely no signs of slowing down anytime soon.

That, in essence, is what Canva is all about.

Canva is a graphic design platform that can be used to create visual content like social media graphics, presentations, posters and more – all via an app that includes templates that make it easy to create the stunning content you need.

The platform itself is available for free, although it does offer paid subscriptions through its “Canva Pro” and “Canva for Enterprise” tiers that unlock additional features for power users. Not only can users create content that immediately exists online, but they can also pay for physical products to be printed and shipped to customers – allowing brands of all types to make meaningful connections with their target audiences.

In April of 2021, Canva reached a $15 billion valuation – simultaneously making its co-founders Melanie Perkins and Cliff Obrecht billionaires. This came less than a year after securing a $6 billion valuation, even though the COVID-19 pandemic was still making its way around the world.

But what may seem like an overnight success was, for those co-founders, anything but. The story of Canva wasn’t always easy – but it is one that can inspire entrepreneurs and businesses professionals everywhere moving forward.

Canva: The Story So Far

The idea that would go on to become Canva began in January of 2012 in Perth, Australia. It was then that Perkins, Obrecht and a third co-founder – Cameron Adams – saw a market that was in desperate need of being filled.

The company began simply enough: They wanted to “make design accessible to all.” It didn’t matter what you actually needed those design services for – logos, business cards, presentations, or something else entirely.

When Perkins and Obrecht were studying in college in Perth, the duo would earn side income by teaching other students various design programs. After determining that some of the platforms offered by companies like Microsoft and Adobe had too much of a learning curve, they decided that there had to be a better way.

But when they couldn’t find it, they decided to create that “better way” themselves.

The duo – now a couple – started an online school yearbook design business, that was then called Fusion Books. They immediately launched a website that let users collaborate and build their profile pages, articles and other content that would then exist in those online school yearbooks. Perkins and Obrecht would then print the yearbooks, after which they would deliver them to schools across the country.

The business was a success, but the pair didn’t want to stop there. They wanted to go bigger, and they had ideas on how to do it.

In 2010, Perkins had an encounter with an investor from Silicon Valley who saw the potential in such an idea. That investor introduced her to a few contacts, at which point they began to develop their idea even further. With the help of a few technology advisors and after the close of their first funding round, Canva was born in earnest – and the rest, as they say, is history.

In its first year after launching, Canva had more than 750,000 active users. Now focused on marketing materials, its revenue increased from an already impressive $6.8 million to an enormous $23.5 million during the 2016/2017 fiscal year alone. Just one year later, in 2018, the company had raised more than $40 million from various investment firms and was already valued at $1 billion.

The point of all this is that there is truly no idea too small (or too niche) to make an impact. Melanie Perkins and Cliff Obrecht were tired of spending time teaching complicated graphics programs to fellow students, so they decided to create a platform of their own to eliminate as much of the “hard work” as possible. That simple idea turned into something much larger than either of them could have imagined.

For an entrepreneur, something like this isn’t just a success story – it’s a critical moment of inspiration to guide all their efforts moving forward.

8 Keys to Creating an Effective Employee Handbook

Most companies have policies or procedures governing their employment practices, but they’re sometimes maintained informally. This can lead to inconsistent application and confusion about employer and employee rights and responsibilities. An employee handbook formalizes those policies so that employees have a written resource to read and reference. Here are some key steps to consider as you create an employee handbook or update an existing one.

#1: Know your history.

Your company’s history, practices, and culture will help set the tone of your handbook and determine what policies to include (see below). Also staying on top of new and changing compliance requirements may necessitate new or updated policies. Think about the information you most need to convey to employees, areas of misunderstanding or confusion, and frequent questions you receive from employees.

#2: Identify required policies.

Although there’s no law that requires a written employee handbook, there are laws that require employers to maintain certain policies in writing. For example, a growing number of jurisdictions require employers to maintain written policies on harassment, discrimination, leave of absence and other time off, and/or workplace safety and health rules. In addition, some state and local laws require employers that maintain an employee handbook to include certain information. For instance, Colorado requires employers with an employee handbook to include a copy of the Colorado Overtime and Minimum Pay Standards (COMPS) Order (or poster). Review all required policies that are applicable to your business and include them in your handbook.

#3: Include other must-have policies.

Even when there isn’t a specific requirement, certain policies are essential for conveying important information. Some examples include:

- A prominent at-will statement in the beginning of your employee handbook (except in Montana, where at-will employment is not recognized). This statement reiterates that, absent certain exceptions, either you or the employee can terminate the employment relationship at any time and for any reason.

- Employment classifications, meal and rest periods, timekeeping and pay, employee conduct, attendance, and punctuality.

- Anti-harassment, nondiscrimination, leave of absence, and workplace safety and health.

#4: Know what policies to avoid.

Just as important as understanding what policies to include is knowing what policies to avoid. These include blanket policies on criminal convictions, withholding final pay until company property is returned, refusing to pay unauthorized overtime/early punch-ins, requiring a doctor’s note for every sick day, prohibiting lawful off-duty conduct, prohibiting employees from discussing their pay with coworkers, probationary/introductory periods, and English-only policies.

#5: Draft policies that reflect company values.

Many employers set a higher standard than what’s required by law. This can be reflected in the language used and the policies selected. For example, to help maintain a harassment-free workplace, many employers will adopt a broader definition of sexual harassment than what’s outlined in federal, state, or local law.

#6: Set the tone.

Employers often include a welcome statement or section in their handbook to help set the tone. This part of the handbook often provides a brief history of the company, defines the company’s mission, explains what makes the company unique (e.g., its core values and work culture), and describes the purpose and importance of the employee handbook.

#7: Create an acknowledgment form.

Each employee should be required to sign and date an acknowledgment stating that they’re responsible for reading, understanding, and complying with the employee handbook. Also, consider including a statement reinforcing the at-will employment relationship. Explain that the employee handbook is not an employment contract, management retains the right to interpret policies, and the company reserves the right to revise the handbook at any time.

#8: Gather feedback.

Ask a few people within your company to provide feedback on your draft handbook and acknowledgment form and then consider having legal counsel review your handbook to help ensure compliance with all applicable laws.

Conclusion:

As you’re building your employee handbook, develop plans for training supervisors on how to interpret and apply the policies, introducing and distributing the handbook to employees, and reviewing and updating the handbook as laws or company practices change.

This story originally published on HR Tip of the Week – a blog providing practical information on hiring, benefits, pay, and more – by ADP®. Learn more about how ADP’s small business expertise and easy-to-use tools can simplify payroll & HR at adp.com.

35 Million: The Total Backlog of Tax Returns The IRS Had At The End Of Tax Season

The Internal Revenue Service has released a midyear report to Congress that details a significant backlog of tax returns dating back to the end of tax filing season, and many of those returns have yet to be processed. While backlogs are not unusual, this year’s is far greater than in previous years.

That’s bad news for those taxpayers who are eagerly waiting for tax refunds. For tax year 2020, roughly 70 percent of the individual returns that have already been processed have resulted in refunds being paid. Those refunds have averaged $2,827.00, but there were still more than 35 million returns for last year that had not yet been addressed by mid-May. An independent advocacy group within the IRS says that at the same point in time the previous year, there were a third the number of backlogged returns as now.

In writing the report, national taxpayer advocate Erin M. Collins said, “For taxpayers who can afford to wait, the best advice is to be patient and give the I.R.S. time to work through its processing backlog. But particularly for low-income taxpayers and small businesses operating on the margin, refund delays can impose significant financial hardships.”

The agency issued a statement indicating that by June 18th, two months after the official filing deadline, almost seven million individual tax returns had been processed. Their work is ongoing continuously, addressing both current returns, those from previous years, and amended returns. More than twice that many are currently being processed.

Backlogs have been a problem in the past, but an evacuation order issued as a result of the pandemic kept IRS employees out of processing facilities, and that and the need to incorporate new tax legislation passed for the 2021 filing season has made things far worse. The agency was also responsible for sending out the third stimulus payment, bringing the total value of payments to $807 billion and the number processed over a 15-month period to 475 million.

While 2019 saw a backlog of 7.4 million returns at the close of tax filing season and 2020’s backlog reached 10.7 million, 2021’s 35 million return backlog has led to several recommendations and objectives being issued to improve things in the future.

A large number of tax returns were processed before the tax filing deadline, and of those 136 million returns, 96 million required that refunds totaling about $270 billion be paid. Both individual returns and business returns are included in the 35.3 million that still need to be processed, and those in the backlog all require additional intervention from an IRS employee in order to be processed.

The Many Benefits of 401(k) Profit-Sharing Plans

If you are an employer looking for an attractive employee benefit that lets you plan contributions around your revenues, consider a 401(K) profit-sharing plan. These plans allow you to make pre-tax deposits to your employees’ eligible retirement accounts after the end of each calendar year, providing the flexibility to determine exactly how much you want to contribute based on your finances and goals.

The Top Five Advantages of 401(K) Profit-Sharing Plans

- You can pay out tax-advantaged bonuses

If your company pays employees year-end bonuses, 401(k) profit-sharing contributions can be an excellent part of that plan. They tax-deductible to your company and don’t increase employees’ taxable income, and are not subject to federal withholding, all while adding to their retirement savings. These value-added benefits make the 401K profit sharing contribution a great way to enhance your annual bonus program. - It adds to your ability to reward Highly Compensated Employees (HCEs)

One of the few drawbacks to 401K plans is the annual deferral limit that the Internal Revenue Service places on contributions. These limits ($19,500 in 2021) prevent Highly Compensated Employees from maximizing the amount that can be contributed to their accounts based on compliance limits for nondiscrimination testing. Profit-sharing plans circumvent these restrictions, allowing a combination of up to $58,000 (with an additional $6,500 catch-up if an employee is over age 50) to be contributed as a bonus. - It provides additional flexibility for budgeting

As nice as it would be to promise high bonuses for year-end, unpredictable revenues make doing so a recipe for disaster. By paying out bonuses in the form of 401(K) profit-sharing contributions, you can assess exactly what you can afford and make the contribution any time before the tax filing deadline – including any extensions you choose to take. Doing so maintains the ability to deduct the contribution on the previous year’s tax return too. - Plans allow contribution vesting

Bonuses and 401(k) plans are valuable recruitment tools, and they can be powerful retention tools when they are structured to vest with the employee’s tenure. Employees considering leaving in a short time frame will lose any portion that has not yet vested. - It can be built into your existing 401(k) plan with no additional work

Signing your company up for a 401(k) plan takes time and effort, but once it is in place you can easily add a profit-sharing plan, and many retirement plan providers will add the program without charging an additional fee.

The disadvantages of profit-sharing plans

As much as our country favors 401(k) plans, including those that incorporate profit-sharing plans, there are a few things that need to be kept in mind.

- There are limits to how much can be contributed for each employee. The total of employee deferrals and employer deposits cannot be greater than 100% of the employee’s compensation.

- You are limited on how much you can contribute for any employee a year. In 2021 that limit is $58,000, or $64,500 for employees over the age of 50.

- Employer contributions may be limited by an employee’s annual compensation. For 2021, no contributions were allowed for employees earning more than $290,000.

- Only contributions of up to 25% of total employee compensation can be deducted by employers.

Acknowledging the contributions that your employees make is an integral part of keeping your workforce morale upbeat, and profit sharing is a powerful tool in support of that goal. If you have questions about how to approach 401(k) profit sharing for your business, contact our office.