Categories for

Vaccine Hesitancy: Why We Have It and How It Affects Employers and Employees

According to a Tufts University survey, six in ten of those surveyed are now vaccinated against COVID-19. However, almost 40 percent of the unvaccinated respondents said they won’t get the vaccine. Only 28.5 percent of the remaining unvaccinated respondents said they will get vaccinated against COVID-19 in the future, with the remaining unvaccinated respondents unable to decide whether they will take the vaccination. With vaccine hesitancy a concern, how can employers encourage more people to get the vaccine?

It is important to understand why some view vaccines skeptically in order to overcome vaccine hesitancy among employees. The Johns Hopkins University Coronavirus Resource Center attributes vaccine hesitancy to a number of factors:

- The first is safety. Since the vaccine was developed faster than most vaccines have been previously, many individuals are concerned about reactions, side effects and quality assurance. More can be read from the CDC VAERS Report.

- The second reason has to do with the vaccine’s effectiveness, and how well it works against the coronavirus.

- The other reasons for hesitancy are due to things like religious beliefs, vaccine phobias and current health issues of the unvaccinated.

This phenomenon is not isolated to the United States. Based on a global survey of 32 nations that Johns Hopkins cites, 98 percent of Vietnamese would get the vaccine, while only 38 percent of those in Serbia would get the vaccine once it’s available.

Navigating Vaccinations in the Workplace

Requesting a Vaccine Exemption Due to Religious Beliefs

Businesses that fall within the purview of Title VII (Civil Rights Act of 1964), must accommodate an employee’s sincerely held religious belief, practice, or observance unless it causes an undue hardship on the business.

The CDC says that once a company is aware of a worker’s “sincerely held religious belief, practice or observance [that stops him from accepting the flu shot], the employer has to provide a reasonable accommodation [except if it causes] an undue hardship.” While this refers to influenza, the reasoning behind it applies equally to an employee expressing their religious objection to a COVID-19 vaccination.

Accommodations for Disabled Employees

According to the Equal Employment Opportunity Commission (EEOC), the Americans with Disabilities Act (ADA) covers employers in the private sector and state and local governments that employ 15 or more workers. The ADA offers guidance for employers when an employee requests to be exempt from a COVID-19 vaccination due to a disability. This Act says that employers can implement a workplace standard specifying that a person cannot “pose a direct threat to the health or safety of individuals in the workplace.”

If, however, this workplace standard either sorts out or will likely sort out a disabled person from meeting the workplace safety standard by being unvaccinated, the employer must demonstrate that such person without a vaccine would pose a direct threat of risk to another person in the workplace that cannot be reduced by reasonable accommodation.

The EEOC believes a direct or proximate threat exists from the unvaccinated person through four tests: length of the danger, the severity of and the type of harm that could occur, the chances of the potential harm that will happen, and proximity of the real harm.

When it comes to determining if a reasonable accommodation exists, the EEOC lists three criteria: the worker’s professional responsibilities, if there is a different job the worker could transition to in order to make the vaccination less necessary, and how serious it is to the company’s function that the worker is vaccinated.

How to Encourage More Vaccinations

The U.S. Chamber of Commerce cautions that for employers who are contemplating mandating their workers take the COVID-19 vaccination, state law varies on how far they can go. However, a good way to get employees vaccinated is by encouraging and not requiring vaccination. Forcing employees to get the COVID-19 vaccination might make workers look for new employment or face a lack of motivation. Depending on the state laws, a vaccine mandate from an employer might lead to a legal battle if employees refuse to get vaccinated or, in rare cases, if an employee dies from the vaccine. One way to incentivize employees to get the COVID-19 vaccine is by offering them a cash payment to do so. Average incentives range from $50 to $500, with most being $100.

Based on recommendations from the Centers for Disease Control and Prevention (CDC), there are many strategies employers can try to help get their employees vaccinated against COVID-19. One recommendation is to have management explain to employees why it’s important to get the vaccination by creating flyers, posters and other forms of communication when staff is entering and leaving the building.

Offering workers, the ability to get vaccinated onsite could encourage people who are on the fence, especially after they see their co-workers get vaccinated. One part of the American Rescue Plan, which passed in 2021, as the Internal Revenue Service (IRS) outlines, permits businesses to claim tax credits if they give their workers paid time off to get vaccinated. This tax credit is eligible for employer reimbursement through paid sick and family leave. It also provides an employer tax credit if employees need time off to recover from any post-COVID-19 vaccine side effects.

Businesses with fewer than 500 employees are eligible for this tax credit for paid sick and family leave that occurs between April 1, 2021, and Sept. 30, 2021. This includes for-profit, tax-exempt organizations and some government employers. Self-employed taxpayers also are eligible for an equivalent tax credit.

Taking the time to encourage workers to get vaccinated, learning how to navigate certain aspects of employment laws and state laws, and making sure to maximize one’s business balance sheet are all essential tools to make the most of 2021 and set up an even better 2022 fiscal year.

Sources

https://www.uschamber.com/co/start/strategy/employee-vaccination-incentives

https://www.cdc.gov/coronavirus

https://coronavirus.jhu.edu/vaccines/report/building-trust-in-vaccination

https://www.irs.gov/newsroom/employer-tax-credits-for-employee-paid-leave-due-to-covid-19

https://www.eeoc.gov/coronavirus

https://www.dol.gov/agencies/whd/pandemic/ffcra-questions

https://www.ada.gov/regs2010/smallbusiness/smallbusprimer2010.htm#whoiscovered

Some Small Businesses Are Recovering. Is Yours?

Intuit recently did a survey documenting the financial losses that many small businesses had experienced since March 2020. Not surprisingly, the report, Intuit QuickBooks Small Business Recovery, found that COVID-19 has had a significant impact on the financial health of U.S. small businesses.

But many of the companies surveyed have proved to be resilient. As of March 31, 2021, 61 percent of them saw an annual revenue increase compared to pre-COVID days.

How would you have answered the survey? If indeed you did suffer financial and personnel losses because of the pandemic, has your business started to rebound yet? If not, there are actions you can take in QuickBooks Online to help in your recovery. Here are some of them.

Transactions: Watch your income and expenses like a hawk.

QuickBooks Online provides excellent transaction-tracking tools that help you document income and expenses.

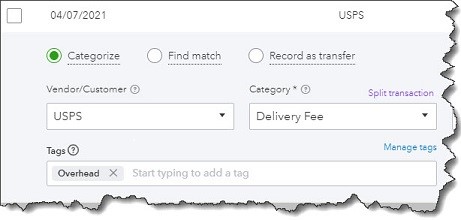

How much time do you spend working with your downloaded transactions? If you take advantage of the excellent tools QuickBooks Online provides, you may notice patterns that you’ll want to explore and modify. For example, are you spending too much in one or more particular areas? When and where is your income dipping?

It’s critical that you connect to as many online financial institutions as possible, so you get a complete picture of your income and expenses. Once you have, click on Transactions in the toolbar, which should open to the Banking page. If you’re only going there to make sure there are no unrecognized entries, you’re missing out on some of QuickBooks Online’s transaction-tracking tools. In the image above, we’ve specified a vendor and chosen a Category and Tags. This will make your reports more meaningful and actionable.

If you don’t know what it means to Find Match, we can show you how that works. It’s a real time saver.

Sales: Make it easier for customers to pay you.

We’ve written about accepting online payments in this column before. It’s especially important if you’re struggling. You may actually be losing sales if you don’t let potential customers pay online through a credit card or bank account transfer. And existing customers may pay faster if they can do business with you in that way.

QuickBooks Payments makes this possible. There are some nominal fees involved, but the potential increase in your income should more than cover them. Let us know if you want us to help you set up a merchant account.

When you set up a merchant account through QuickBooks Payments, you may find that your customer base will grow, and existing customers will pay faster.

Expenses: Categorize expenses with tax time in mind.

You’ve probably already filed your 2020 income taxes, but we’re well into 2021, and it’s not too early to start thinking about your current tax situation. QuickBooks Online helps you track your income carefully, but it’s equally important to make sure you know what your tax-related expenses are. You want to get every deduction and credit you can. So when you’re looking at transactions, like we described above, make very certain that you’re assigning the correct categories to each of them.

We can help you run reports on a quarterly basis that should be of help when you make estimated tax payments. That way, you may be able to reduce your quarterly obligation during the 2021 tax year and won’t have to wait until you file in 2022 to see savings.

Time: Make sure your billable hours are billed.

Unless you have an organized, easy-to-use method for tracking billable time, some hours are likely to fall between the cracks. QuickBooks Online provides effective tools in this area. As you go through your downloaded transactions, you may see expenses that can be billed to a customer. Select the Customer/project and check the Billable box so you’ll be able to include it on their next invoice.

You can mark expenses as billable to customers in your Transactions register.

As you create time entries for you and/or your employees, you can also mark those hours as billable.

Reports: Run basic, critical reports regularly.

You can’t know how your business is doing financially unless you create reports. Besides the quarterly and standard financial reports we can run and analyze for you, you can—and should—be generating reports yourself through QuickBooks Online. Here are some of the ones we suggest:

- Budget vs. Actuals. If you’ve put the time and effort into creating a budget, it’s critical that you gauge your progress regularly and make adjustments as needed.

- Open Invoices. Who have you billed that hasn’t paid?

- Accounts Receivable Aging Detail. Who owes you, and how far behind are they?

- Sales by Product/Service Detail. What is selling well and what isn’t? You can make decisions about your product and service lines by viewing this report. This is especially important when your sales are sluggish.

- Business Snapshot. This is a series of charts and lists that provides a quick visual overview of key data.

QuickBooks Online can’t, of course, revive your business if the pandemic has created conditions that are out of your control. But that shouldn’t stop you from controlling what you can, no matter what your situation is. It was designed not only to automate and streamline your daily accounting work, but also to provide the information you need as you evaluate your present situation and plan for the future. Please call on us if you need help making optimal use of QuickBooks Online.

7 Different Types of Income Streams for Your Business

No matter what type of business you operate, you rely on having a predictable flow of income to keep your bills paid. If you only have a single source of income and it suddenly falters, you’re going to be in trouble. Having more than one income stream is an insurance policy against economic disaster. It provides a cushion to keep you afloat if your business suddenly falls off. Though some types of businesses have a clearer path to expanding their income streams then others, with a little creativity you can identify new sources of revenue that can add stability, save you from a downturn, and even add to your bottom line.

The Difference Between Active and Passive Income Streams

There are several different types of income streams, all of which fall into the category of either active or passive. If you are making something, selling something, or providing a service of some kind in exchange for direct payment, that is active income. While passive income also generates revenue, the payment is not as connected to the original work. A good example of someone earning passive income would be an author’s book sales. While months or even years of work went into the book’s publication, the income generated by the book’s sales after publication is passive. They go on without the author lifting a finger, with income deposited into their bank account for years after, and even following their death.

How to Add New Income Streams to your Business

Adding new income streams to your business is known as diversification, and it is not as hard as it sounds. Any type of business can create new sources of revenue. A dog grooming salon can start to sell dog toys, or clothes, or food. Supermarkets can add pharmacies, hair salons can add spa services like massage and skincare. Many retailers have created online stores that sell their products.

One of the most famous examples of income stream diversification can be seen in Sir Richard Branson’s iconic Virgin brand. Though it began as a record store, the company has branched out into a wide range of products and services, including jewelry, cruises, mobile phone service, and even an airline. Though you may not dream quite as grandly as Sir Richard, you still have options available to you. Even people who feel limited by being skilled in a specific industry, like plumbers or electricians, can generate additional revenue streams by making videos of themselves teaching basic home repair skills and uploading them for monetization on YouTube, or offering to teach classes at the local high school or at homeowners’ association meetings.

Different Income Streams

To help you identify alternative sources of income for yourself or your business, here is a list of 7 different types of income streams:

- Capital Gains – This is income that comes from selling stocks and other assets at a profit. Though it is extremely satisfying to buy something for a low price and sell high, the taxes on capital gains can quickly dampen your enthusiasm for this as a source of income. Capital gains are also reliant on market trends and are therefore unpredictable.

- Dividends – Dividends are payments that are distributed to owners of shares in a company. The more shares you own and the more profitable a company is, the more dividends you are likely to receive. They can be an excellent source of passive income.

- Earned Income – Earned income is the money that you make from your job. It is straightforward and active and is almost always the primary source of income.

- Interest Income – This is passive income earned from investment or savings. The money that you earn in an IRA, a savings account, or by investing in bonds is interest income.

- Profit Income – Profit income is active income that is the goal of all businesses. It represents the difference between the cost of selling a service or product and a higher price that you sell it for. The greater your profit margin and volume, the more profit income you make.

- Rental Income – If you own property that you are not using and are willing to have somebody else use the space, you can offer to rent it. Rental income represents an excellent source of passive income, but it requires making an initial investment in the property itself, and there are costs and tax liabilities involved.

- Royalty Income – Royalty income is paid to people who create something and then get paid every time that it is used. To earn royalty income, you need to have established your ownership rights and created a marketing plan through which you will get paid. Examples are the monies paid to musicians and authors when their music is played or their books are sold.

There’s an old adage about needing to have money to make money, and that is true of some of these — you aren’t going to be able to earn royalties if you haven’t published music or literature, and you aren’t going to be able to earn rental income if you don’t have a property to rent. Still, it is a good idea to familiarize yourself with all of the options so that you can keep your mind open to all of the opportunities. The more income streams you can add to your business, the less risk of financial trouble when one revenue source suffers a downturn.

If you have any questions about income streams as an individual taxpayer or business owner, please contact us.

How Biden’s Proposed American Families Plan Might Affect You

President Biden presented his proposed American Families Plan (AFP) during his Joint Session of Congress address on April 29, 2021. What follows is an overview of what is included in the plan. But this is only his wish list; Congress will need to draft proposed legislation that will have to pass in both the House of Representatives and the Senate before becoming law. With a price tag of more than $1.8 trillion, many on both sides of the political aisle think the plan is too expensive. As with virtually all legislation, the provisions will be debated, altered and deleted during Congressional negotiations. The final bill, if passed, may be quite different than the original proposed version.

BENEFITS

Education Benefits – The AFP primarily incorporates education benefits that, if passed, would add four years of free public education and provide federal funds to certain higher education institutions. More specifically, it would address:

- Pre-Kindergarten Education – Provide free universal preschool to all three- and four- year-olds.

- Community College Education – Provide two years of tuition-free community college education, including for DREAMers.

- Pell Grants – Increase Pell Grants by approximately $1,400 to assist low-income families and DREAMers.

- College Retention and Completion Rates – Include a $62 billion grant program to invest in completion and retention activities at colleges and universities (particularly community colleges) that serve high numbers of low-income students. States, territories and tribes will receive grants to provide funding to colleges that adopt innovative, proven solutions for student success.

- Subsidized Tuition – For families earning less than $125,000, provide two years of subsidized tuition at historically black colleges and universities and other minority-serving institutions. The plan would expand and create additional grants for these schools to strengthen their academic, administrative and fiscal capabilities, including by creating or expanding educational programs in high-demand fields such as STEM, computer sciences, nursing and related health care.

Education, Teachers and Educators – The AFP includes several provisions to increase college retention and completion rates, address teacher shortages, improve teacher preparation and strengthen pipelines for teachers of color. It would double scholarships for future teachers from $4,000 to $8,000 per year while they are earning their degree and would also help current teachers earn in-demand credentials.

Child Tax Credit – The President is proposing that the Child Tax Credit increases included in the American Rescue Plan Act (ARPA) be made permanent. The ARPA increased the Child Tax Credit from $2,000 per child to $3,000 per child six years old and above and $3,600 per child under six years old. It also made 17-year-olds eligible children for the credit and made the credit fully refundable and payable periodically during the year. These changes were for 2021 only. The AFP proposal would extend the ARPA increases through 2025 and make the refundability permanent.

Child & Dependent Care Tax Credit – The ARPA, for 2021 only, made this credit fully refundable and provided a credit equal to 50% of the expenses before phaseout. The maximum amount of expenses that can be used to compute the credit was increased to $8,000 for one qualified individual and $16,000 for two or more qualified individuals. As under prior law, a dependent child qualifies if they are under the age 13. The maximum credit is $4,000 (50% of $8,000) for one eligible individual and $8,000 (50% of $16,000) for two or more eligible individuals. The AFP would make these changes permanent.

Earned Income Tax Credit (EITC) for Childless Workers – The ARPA essentially tripled the EITC for childless workers for 2021 only. The one-year change increased the maximum credit from $543 to $1,502. Biden is asking Congress to make this increase permanent.

Paid Family Leave – The AFP would create a program that would ensure workers receive partial wage replacement to take time to bond with a new child, care for a seriously ill loved one, deal with a loved one’s military deployment, find safety from sexual assault, stalking or domestic violence, heal from a serious illness of their own or take time to deal with the death of a loved one. It would guarantee twelve weeks of paid parental, family and personal illness/safe leave by year 10 of the program and also ensure that workers get three days of bereavement leave per year starting in year one. The program would provide workers up to $4,000 a month, with a minimum of two-thirds of average weekly wages being replaced, rising to 80 percent of average weekly wages for the lowest-wage workers.

Health Insurance – The AFP would extend the expanded ACA health insurance premium tax credits included in the ARPA that lowered health insurance costs by an average of $50 per person per month for nine million people, and it would enable four million uninsured people to gain coverage. In addition to other provisions, individuals would be able to enroll in Medicare at age 60.

TAX INCREASES TO PAY FOR THE BENEFITS

Corporate Tax Rate – The proposal would increase the corporate tax rate from 21% to 28% (the rate was 35% before the 2018 tax reform).

Individual Marginal Tax Rates – The proposal would increase the top marginal tax rate from 37% to 39.6% for taxpayers with taxable income in excess of $400,000. That may be an oversimplification since tax rates take into account a taxpayer’s filing status. According to Jen Psaki, the White House press secretary, the 39.6% rate would apply to families with a taxable income of $509,300 or greater and single individuals with a taxable income of $452,700 or greater. Also, keep in mind that tax rates are adjusted for inflation annually.

Capital Gains Tax – The proposal would end the lower maximum capital gains rates for households making over $1 million (the top 0.3 percent of all households), thus having them pay the same 39.6% rate on all their income and equalizing the rate paid on investment returns and wages.

Basis Step-up – Currently, when assets are inherited, their basis in the hands of the beneficiary is the fair market value of the asset at the date of the decedent’s death. Taxable gain when an asset is sold is the difference between the selling price and the asset’s basis. Thus, under current law, assets can be transferred to beneficiaries without any income tax liability for the beneficiaries.

Under the AFP, any basis step-up would be eliminated for gains in excess of $1 million ($2.5 million per couple when combined with existing real estate exemptions), ensuring the gains will be taxed if the property is not donated to charity. The reform would be designed with protections so heirs will not have to pay taxes on family-owned businesses and farms given to them if they continue to run the business.

Carried Interest – Carried interest is a share of a private equity partnership’s or fund’s profits that serves as compensation for fund managers. Because carried interest is considered a return on investment, currently it is taxed at a capital gains rate and not an ordinary income rate. The proposed tax changes would eliminate carried interest, and thus the income would be taxed at ordinary rates.

Like-kind Exchange for Real Estate – Sec 1031 of the Internal Revenue Code allows taxpayers to exchange real estate used in business or for investment for other business or investment real estate and avoid taxation by deferring the gain in the replacement property. The proposed plan would eliminate Section 1031 like-kind exchanges for real estate investors when they exchange property on gains greater than $500,000.

Excess Business Losses – An “excess business loss” is the excess (if any) of the taxpayer’s aggregate deductions for the tax year that are attributable to trades or businesses of the taxpayer (determined without regard to whether or not the deductions are disallowed for that tax year) over the sum of

(i) the taxpayer’s aggregate gross income or gain for the tax year attributable to those trades or businesses plus

(ii) $250,000 (200% of that amount for a joint return (i.e., $500,000)). This amount is adjusted for inflation.

The current limitation is through 2021. The proposed changes would permanently extend the current limitation restricting large excess business losses.

Medicare Tax – Currently there is a 2.9% Medicare surtax on earned income (wages, self-employment) for taxpayers whose earnings exceed $250,000 (joint), $125,000 (married filing separate) or $200,000 (others). When added to the regular 0.9% Medicare rate, the total paid is 3.8%. There is also a 3.8% Medicare surtax on net investment income that applies when the taxpayer’s income exceeds $250,000, $125,000 or $200,000, depending on their filing status. Biden’s plan would apply the 3.8% surtax consistently to those with income over $400,000.

Tax Preparer Regulation – The proposal would give the IRS the authority to regulate paid tax preparers. Currently, CPAs and Enrolled Agents have continuing education requirements, as do tax preparers in Oregon and California. However, in other states, individuals can prepare tax returns without any oversight, which results in high error rates. These unregulated preparers charge taxpayers large fees while exposing them to costly audits.

Compliance – The proposal would substantially raise the IRS’s budget to increase tax compliance of high-income earners and large corporations, businesses and estates.

Bank Information Reporting – The proposal would require financial institutions to report to the IRS how much money came into and out of individuals’ and businesses’ accounts each year.

This material is a synopsis of key provisions of the President’s American Families Plan but does not include all proposed changes. Consult the White House fact sheet for additional provisions and details.

Entrepreneur Success Stories: Zapier

Success leaves clues.

Zapier is a software company founded in 2011 by Wade Foster, Bryan Helmig, and Mike Knoop. Zapier provides a service that helps end-users automate the integration of online applications that they use.

Let’s take a look at a behind-the-scenes software integration company that has taken the industry by storm.

HOW ZAPIER GOT THEIR START

Before becoming a company valued at over $5 billion, Wade Foster (CEO) and Bryan Helming (CTO) were members of a jazz quartet, playing gigs together in their hometown of Columbia, Missouri.

In addition to their love for music, they discovered that they both also had a passion for creating web applications and began working on projects together.

In September 2011, they came up with an idea that would change the course of their lives. They decided to start a company that helped end-users to integrate two different software applications. To help get their idea off the ground, they enlisted a third co-founder, Mike Knoop (CPO) and went to work.

They created the first iteration of their software application (known then as API Mixer) and entered a local start-up competition. Their idea won, and they knew they were on to something.

They continued to develop their idea and submitted it to Y Combinator, where they were initially rejected. Foster, Helmig, and Knoop refused to take no for an answer and continued to submit their application to Y Combinator until they were finally accepted in 2012. At that time, the project included integrations with 34 applications. Today, that number is over 3,000 integrations, and they have more than 300 application partners.

During their early stage, they were able to secure $1.3 million in Series A funding from investors and within two years, they reached profitability. This was the only venture capital funding that they’ve accepted thus far, though they have received numerous offers along their journey.

Zapier has gone on to be awarded the #1 company in the early-stage category as evaluated by top venture funds in the industry.

KEYS TO SUCCESS

Going from zero to a $5 billion company within a decade is no easy feat. Zapier’s success can be attributed to many of the decisions that the founders have made along the way.

Building Relationships with the Zapier User Base

Zapier believed that building relationships were crucial to helping them to build and grow their user base. Foster, Helmig, and Knoop started by visiting online forums of larger software applications such as Dropbox and Basecamp and seeking users who were frustrated with their inability to use the functionality of one application along with another, often having to repeat the same tasks across applications. The Zapier team would reach out to these users and offer to help them resolve their issues. In the early stages of the company, this how they generated their first customers. Customer service continues to be a foundational part of who Zapier is as a company.

Customer-Centric Values

As an employee of Zapier, each team member will participate in the customer support function. Whether an employee is in HR or IT, the founders believe that hearing first-hand about how customers are experiencing the product and understanding their frustrations will help to create a better product and experience.

Teamwork is Key

Zapier has been a remote company since its founding. With team members across the company and the globe, it is important for them to be able to communicate with one another to ensure each team member is on the same page. They do this by sharing information across multiple channels and multiple times to ensure that important ideas are communicated. Transparency is one of their keys to success.

Tell the Customer’s Story

As the function of the Zapier software is to connect other software applications, the company will not be front-of-mind if working properly. As a result, Zapier has had to be very deliberate in how they reach out to current and potential customers.

One part of their marketing efforts through their blog is to share the success stories of their clients. Zapier interviews customers, identify pain points that have been resolved through the application and uses this as a guide to assist other customers who might be experiencing the same issue.

This attention to detail in addressing customer concerns and success has helped the company grow from its first customers back in 2012 to its current user base of over 600,000 users.

Zapier’s success reveals how dedicated client focus can have a huge impact on the bottom line.

If you have any questions about turning your business into a success story or you would like to learn more about our services, please feel free to contact us for more information.

Here’s What Happened in the World of Small Business in April 2021

Here are five things that happened this past month that affect your small business.

1) President Biden announced tax credits for COVID-19 vaccination paid time off.

The President announced on April 21st “tax credits for certain businesses that pay employees who take time off to get COVID-19 shots, a new effort to involve corporate America in his vaccination campaign.” The tax credits will be applicable for businesses with fewer than 500 employees. (Source: Reuters)

Why this is important for your business:

Providing your employees with paid time off to get their vaccine will now be covered by the government, so you can encourage vaccinations if you choose without taking on the cost of offering additional PTO.

2) Workers at an Amazon warehouse in Alabama voted not to unionize, but the company is being accused of violating laws.

The union vote we discussed last month has been completed, and workers at the Amazon fulfillment center in Bessemer, Alabama voted not to unionize. This was seen as a win for Amazon; however, the union that led the drive “has filed challenges over the vote, saying the company violated legal restrictions throughout the election.” (Source: The Wall Street Journal)

Why this is important for your business:

This union push caught the attention of workers, unions, businesses, and government officials, and the story isn’t over yet. Additionally, other groups across the US have already started announcing their goals to unionize, inspired by the push in Bessemer. No matter your views on organized labor, keep paying attention to this story.

3) Businesses across the world are bracing (and hoping) for an impending post-pandemic “spending boom.”

Could we be in the beginning stages of a global spending spree? “Consumers around the world have amassed an extra $5.4 trillion in savings since the coronavirus pandemic began, setting the stage for a spending boom that could power a strong uplift in economic growth this year.” (Source: CNN Business)

Why this is important for your business:

Revenue, revenue, revenue.

4) Small businesses can get another $500k from the Small Business Administration (SBA).

Beginning April 6th, the SBA expanded its Economic Injury and Disaster Loan (EIDL) program. “Small businesses who originally took out an EIDL loan for up to $150,000 for six months can extend that loan for up to 24 months and receive additional funds for a total of $500,000 in relief.” Additionally, the deferment period for both Paycheck Protection Program (PPP) and EIDL loans was extended through 2022. (Source: Yahoo! Finance)

Why this is important for your business:

If your small business is still struggling financially and you need additional funding, the EIDL expansion could help.

5) The conversation around corporate taxation (and large firms who pay $0 in taxes) is growing louder.

A report from the nonpartisan Institute on Taxation and Economic Policy found that “55 of the largest firms in the country used a complex roadmap of tax breaks and loopholes to bring their tax bill down to zero, despite turning millions, or even billions in profit.” (Source: Fast Company)

Why this is important for your business:

This finding has added fuel to the conversation around corporate taxation – or a lack thereof – in the US. Keep an eye on the public discourse and any moves made by politicians to speak on this topic in the coming months.

SBA Raises Loan Limit For COVID-19 EIDL Loans to $500,000

As U.S. businesses continue to recover from COVID-19’s economic devastation, the U.S. Small Business Administration (SBA) is expanding loan opportunities. The agency announced that beginning the week of April 6th, nonprofits and small businesses will be able to borrow up to $500,000 for up to 24 months. This expansion of the COVID-19 Economic Injury Disaster Loan (EIDL) program more than triples the existing limit of six months and a maximum loan amount of $150,000.

In a news release announcing the change, SBA Administrator Isabella Casillas Guzman said, “More than 3.7 million businesses employing more than 20 million people have found financial relief through SBA’s Economic Injury Disaster Loans, which provide low-interest emergency working capital to help save their businesses. However, the pandemic has lasted longer than expected, and they need larger loans.”

Businesses that had already applied for a COVID-19 EIDL loan need not worry about reapplying, as all applications in process will automatically be considered for the increased amounts. Similarly, instructions will be published to allow those who have already been approved for a loan to apply for the expanded amounts. A loan increase can be requested via SBA.gov, and an email will go out to all previously approved borrowers containing the same information.

The COVID-19 EIDL program has been extremely successful, with over $200 billion in loans already approved by the SBA. Small businesses, including independent contractors and sole proprietors, have been provided 30-year maturity loans at a 3.75% interest rate, while not-for-profits will pay 2.75% in interest.

In more good news for borrowers, on March 12th the SBA announced that borrowers for all disaster loans, including the COVID-19 EIDL loans, would be provided extended deferment periods. Interest will still accrue on all outstanding loan balances, so though payments are not required until 2022, borrowers do have an incentive to begin paying their balance off sooner.

If you have any questions about the EIDL loan limit expansion and how it could affect your business, please contact our office.

IRS to Automatically Adjust Prior Filed 2020 Returns with Unemployment Income

The IRS announced on March 31, that it will take steps to automatically refund money this spring and summer to people who filed their tax returns reporting unemployment compensation before the recent law change made by the American Rescue Plan Act.

The American Rescue Plan Act, signed on March 11, allows each taxpayer who earned less than $150,000 in modified adjusted gross income to exclude up to $10,200 of unemployment compensation from taxation. Since it applies to each taxpayer, married couples where both spouses received unemployment benefits may be able to exclude up to $20,400 if married filing status. The legislation excludes only 2020 unemployment benefits from taxes.

Because the change occurred after some people filed their taxes, the IRS will take steps in the spring and summer to make the appropriate change to the returns of these individuals, which may result in a refund. The first refunds are expected to be made in May and will continue into the summer.

For those taxpayers who already have filed and figured their tax based on the full amount of unemployment compensation, the IRS will determine the correct taxable amount of unemployment compensation and tax. Any resulting overpayment of tax will be either refunded or applied to other outstanding taxes owed.

For those who have already filed, the IRS will do these recalculations in two phases, starting with those taxpayers eligible for the up to $10,200 exclusion. The IRS will then adjust returns for those married filing jointly taxpayers who are eligible for the up to $20,400 exclusion and others with more complex returns.

There is no need for taxpayers to file an amended return unless the calculations make the taxpayer newly eligible for additional federal credits and deductions not already included on the original tax return.

For example, the IRS can adjust returns for those taxpayers who claimed the Earned Income Tax Credit (EITC) and, because the exclusion changed the income level, may now be eligible for an increase in the EITC amount which may result in a larger refund. However, taxpayers would have to file an amended return if they did not originally claim the EITC or other credits but now are eligible because the exclusion changed their income.

If you have questions, please give our office a call.

7 Ways to Save 10K a Year

If you’re scratching your head and wondering if we’ve lost our minds, please keep reading. You can do this. All you need to do is plan your steps – and stick to it. After all, Confucius says, “A journey of a thousand miles begins with a single step.” So let’s get moving.

Save Before You Spend

This might well be the opposite of what you do: you get your weekly or monthly paycheck, determine what expenses are ahead, then dedicate what’s left to savings. To save $10,000, the first thing to do is put away the money you’ve designated to reach your goal first (50 percent? 25 percent?), then live off the amount that’s left. Yes, it’s backwards, but in the end it’s the way forward to realize your 10k dream.

Set Up a High-Interest Savings Account

So that cash you’ve set aside? Deposit it into a savings account that will make your money grow. Several good options are Vio Bank (APY: 0.57 percent), Comenity Direct (APY: 0.55 percent), and Ally Bank (APY: 0.5 percent). This could mean the difference of hundreds (or even thousands) of dollars of interest over time.

Baby Step Your Way There

Break your goal into small chunks. Let’s say your monthly savings goal to get to 10k is $500 a month. If that’s too overwhelming, break it into two $250 chunks. If that’s too much, $125 a week, and so on. You can even parse out per day: $500 divided by 30 days in a month = $16. You can do this!

Start a Side Hustle

If you find you can’t make the amount you want to save each month and you aren’t able to tailor your expenses to fit your goal, start a side gig. For instance, if you’re able-bodied, consider helping people move and/or helping them assemble furniture. Other options include babysitting, food delivery, taking market research surveys, running errands and more. TaskRabbit is a great resource to find all kinds of ways to increase your income.

Cut Unnecessary Expenses

Look closely at your expenditures. Decide if you’re really reading that magazine and think about canceling the subscription. Pack a lunch and/or cook in for dinner. Call your internet and cell phone provider to see if they have a better deal. If you want to add an extra $1,000 to your savings each year, all you have to do is cut out $84 a month. This is doable.

Commit to a Budget

Everything that means something requires hard work and commitment. Take an afternoon, put it all down on paper, and promise to live within a dedicated financial scope. Compare your short-term gratification to your long-term financial goal. Imagine how good you’ll feel when you’ve saved $10,000. The power of visualization works.

Track Your Progress

If you’re feeling overwhelmed along the way, it pays to go back and see how far you’ve come – and we’re talking literally see it. Make your milestones visible. Hang a chart in your kitchen and color it in when you make a deposit. Or if you’re more analytical, create a spreadsheet, but keep it on your desktop. Checking this every day will help keep you on point.

Saving for a goal like this can be fun and even exciting. All you have to do is be mindful and make a conscious decision to follow your plan, and your 10k dream will be realized before your know it.

Sources

https://bethebudget.com/how-to-save-10000-in-a-year-or-less/

New Rules and Ways to Use HSAs/FSAs

People who own a high-deductible health insurance plan may have the option to open a health savings account (HSA). HSA users can contribute pre-tax income to the account and invest the money for tax-free growth in a variety of mutual funds, stocks, and exchange-traded funds (ETFs).

The funds may be withdrawn tax-free when used to pay for qualified expenses, such as the plan’s high deductible, copayments, and coinsurance. The funds can also be used to purchase a wide range of health-related products.

A recent poll found that 40 percent of respondents who have access to a health savings account do not fully understand them. Perhaps that is why legislation passed last year that increased eligible uses of HSA funds largely went under the radar. The CARES Act included a provision that greatly expanded the number and types of health-related products and services that can be paid for with money from an HSA or an employer-sponsored Flexible Spending Account (FSA). The following list includes many of the newly eligible expenses (note: some require a Letter of Medical Necessity (LMN) from a licensed provider):

- Over-the-counter medications, such as those for fever, cold and flu, headache, muscle aches, acid, heartburn and indigestion relief, allergy and sinus relief, and diarrhea and constipation relief

- Toothache relief items

- Skin and rash ointments, medicated body lotions

- Rubbing alcohol

- Thermometers

- Band-Aids and bandages

- Kinesiology tape

- Hot and cold therapy packs, cooling headache pads

- Eye drops

- Facial cleansers, face wipes

- Prescription acne medication and over-the-counter acne treatments

- Sunscreen and SPF moisturizers (including expensive anti-aging facial lotions with SPF protection)

- Lip balm for sun protection and chapped lips

- Sleep and snoring aids

- Smoking cessation nicotine gum, patches, lozenges, inhalers, and nasal sprays

- Prescription sunglasses

- Humidifiers, air purifiers, and filters

- Dietician fees

- Some mental health treatments and services

- Prescription hormone replacement therapy

- Birth control pills

- Pregnancy tests

- Fertility tests

- Fertility treatments such as in vitro fertilization, intrauterine insemination, fertility medication, the temporary storage of eggs or sperm

- Birth classes and medically certified doulas

- Breast pumps, breastfeeding classes, absorbent breast pads, and breast milk storage bags

- Baby monitors and potty-training undies

- Feminine care items, such as pads, tampons, cups, and sponges

- DNA/Ancestry kits

In 2021, the contribution limit for a health savings account is $3,600 for individuals and $7,200 for families; anyone age 55 or older can make an additional $1,000 annual contribution.

Just recently, the IRS published guidelines for employers regarding the use of Flexible Spending Account funds. Because of social distance guidelines and shutdowns in 2020, many people continued to work from home and contribute to their FSA but were unable to use those funds, which are generally designed to be used in the year saved (or otherwise lost).

The new guidelines allow employers to carry over or extend the grace period for unused health and/or dependent care FSA funds to the immediately following plan year. This new rule is retroactive for the 2020 and 2021 plan years. Note that while the IRS permits these new extension rules, it is up to employers to decide what they want to do.