Categories for

10 Red Flags For IRS Audits

Even though the overall IRS audit rate is currently low historically, it’s expected to increase as a result of provisions in the Inflation Reduction Act signed into law in August. So it’s more important than ever for taxpayers to follow the rules to minimize their chances of being subject to an audit. How can you reduce your audit chances? Watch for these 10 red flags that can trigger IRS scrutiny:

- Large charitable donations. The IRS can reference data providing average charitable deductions based on various income levels. If you’re above average for your category, you might call attention to yourself. This is especially true if you’ve deducted charitable gifts of appreciated property. So make sure your donations are all properly substantiated, including by independent appraisals if required.

- Gambling losses. Generally, you can deduct losses up to the amount of your winnings on your personal return, but you must have proof to back up your claims. If your gambling activities rise to the level of professional gambler, you might be able to deduct a loss from other income, but the IRS often contests this tax treatment. Recognize the risks.

- Unreported income. It’s easy to miss income that might fall through the cracks, such as interest and dividends as well as nonemployee compensation from Form 1099-NEC. If you fail to report the income, the IRS may uncover a discrepancy with the forms it receives. Be sure to provide your tax professional with all forms you receive.

- Rental income and deductions. You don’t want the IRS to find that you played fast and loose with the rules for rental properties. Showing a loss for the year despite a high rental rate could trigger an inquiry. Generally, you may use up to $25,000 of loss to offset income from nonpassive activities, but you must meet specific participation requirements. Check with your tax advisor to see if you’re on firm ground.

- Home office deductions. If you use a portion of your home regularly and exclusively for your business, you may be able to deduct the expenses and depreciation associated with the space. Usually, the greater the business percentage claimed for use of the home, the greater the audit risk. Employees who work from home (as opposed to self-employed people) currently can’t claim a home office deduction. Now that more people are working from home, the IRS may look for taxpayers trying to bend the rules.

- Casualty losses. Despite recent legislative changes restricting casualty loss deductions, you can still write off losses to personal property sustained in a federally designated disaster area. But be aware that the IRS may scrutinize appraisals to determine if you’re inflating a disaster-area loss.

- Business vehicle expenses. The IRS often flags returns with large deductions for business vehicles, especially if they reflect double-digit depreciation allowances. Briefly stated, you’re required to keep a contemporaneous log of your driving activities, along with proper substantiation. Collect all the proof needed to withstand an IRS challenge.

- Cryptocurrency transactions. This is a relatively new potential audit target. The IRS now specifically asks on your return if you’ve bought or sold cryptocurrency. If you’ve answered yes, be prepared to substantiate the transaction information.

- Day trading activities. Most taxpayers offset capital gains and losses from securities sales on Schedule D of their personal tax returns. But claiming to be a “day trader” may help you benefit from favorable tax provisions, including deductions for specific expenses. If you do this, consult with your tax advisor to ensure you’re ready to respond to any IRS inquiries.

- Foreign bank accounts. Checking the box on Schedule B that indicates you have a foreign bank account could increase your chances of an audit. But failing to check the box when you should do so may also trigger an audit. The IRS matches up information it receives on foreign bank accounts. Generally, a taxpayer must file a Report of Foreign Bank and Financial Accounts (FBAR) if the aggregate value of assets in foreign bank accounts exceeded $10,000 during the prior year.

Of course, this isn’t the end of the list. There are many other potential audit triggers, depending on a taxpayer’s particular situation. Also, keep in mind that some audits are done on a random basis. So even if you have no common triggers on your return, you still could be subject to an audit (though the chances are lower).

With proper tax reporting and professional help, you can reduce the likelihood of triggering an audit. And if you still end up being subject to one, proper documentation can help you withstand it with little or no negative consequences.

©2022

Selling Your Home?

Be sure you understand the home sale gain exclusion

If you’re thinking about selling your home, it’s important to determine whether you qualify for the home sale gain exclusion. The exclusion is one of the most generous tax breaks in the tax code, so be sure to review its requirements before you sell.

Exclusion requirements

Ordinarily, when you sell real estate or other capital assets that you’ve owned for more than one year, your profit is taxable at long-term capital gains rates of 15% or 20%, depending on your tax bracket. High-income taxpayers may also be subject to an additional 3.8% net investment income (NII) tax. If you’re selling your principal residence, however, the home sale gain exclusion may allow you to avoid tax on up to $250,000 in profit for single filers and up to $500,000 for married couples filing jointly.

Don’t assume that you’re eligible for this tax break just because you’re selling your principal residence. If you’re a single filer, to qualify for the exclusion, you must have owned and used the home as your principal residence for at least 24 months of the five-year period ending on the sale date.

If you’re married filing jointly, then both you and your spouse must have lived in the home as your principal residence for 24 months of the preceding five years and at least one of you must have owned it for 24 months of the preceding five years. Special eligibility rules apply to people who become unable to care for themselves, couples who divorce or separate, military personnel, and widowed taxpayers.

Limitations apply

You can’t use the exclusion more than once in a two-year period, even if you otherwise meet the requirements. Also, if you convert an ineligible residence into a principal residence and live in it for 24 months or more, only a portion of your gain will qualify for the exclusion.

For example, John is single and has owned a home for five years, using it as a vacation home for the first three years and as his principal residence for the last two. If he sells the home for a $300,000 gain, only 40% of his gain ($120,000) qualifies for the exclusion, and the remaining $180,000 is taxable. (Note: Nonqualified use prior to 2009 doesn’t reduce the exclusion).

Partial exclusion

What if you sell your home before you meet the 24-month threshold due to a work- or health-related move, or certain other unforeseen circumstances? You may qualify for a partial exclusion.

For example, Paul and Linda bought a home in California for $1 million. One year later, Paul’s employer transferred him to its New York office, so the couple sold the home for $1.2 million. Paul and Linda didn’t meet the 24-month threshold but, because they sold the home due to a work-related move, they qualified for a partial exclusion of 12 months/24 months, or 50%.

Note that the 50% reduction applied to the exclusion, not to the couple’s gain. Thus, their exclusion was reduced to 50% of $500,000, or $250,000, which shielded their entire $200,000 gain from tax.

Crunch the numbers

Before you sell your principal residence, determine the amount of your home sale gain exclusion and your expected gain (selling price less adjusted cost basis). Keep in mind that your cost basis is increased by the cost of certain improvements and other expenses, which in turn reduces your gain. Also, be aware that capital gains attributable to depreciation deductions (for a home office, for example) will be taxable regardless of the home sale gain exclusion.

© 2022

What is Datafication, and Should Business Leaders Take Notice?

Data has become a primary asset for businesses today. Consequently, the survival of a business in our data-driven environment is highly dependent on the ability to have total control over data storage, extraction, and manipulation.

As businesses continue being bombarded with vast volumes of data, datafication has become a big trend that provides a solution to turn data into quantifiable, usable, and actionable information.

What is Datafication?

The term datafication was coined by Kenneth Cukier and Victor Mayer-Schöenberger in 2013 when they explained it as the transformation of social actions into quantifiable data.

Today, much data is collected at the point of contact with any technology device. Aside from data such as text, images, and numbers, there are logins, passwords, device activity logs, clicks, interaction times, and more. Datafication helps translate all of these human activities into data, which is then repackaged in a form that offers value.

In business, datafication means converting every activity of a business model into actionable data. This has been enabled by a rise in technologies such as artificial intelligence, machine learning, big data analytics, and predictive analytics.

It’s worth noting that datafication is not the same as digitization. While datafication is about taking all aspects of life and turning them into a data format, digitization involves converting analog content, such as images and text, to a digital format.

Examples of Datafication in Real Life

There are various ways datafication has been applied in real life, including:

- Social media platforms – a lot of data is found on social platforms through profile updates, preferences, reactions, comments, and posts. Such information is used for customer profiling.

- Ad personalization – tech giants such as Facebook, Google, Apple, and Amazon are already using collected data in their storage to personalize their ads and target potential customers.

- In customer relationship management – data collected through language and tone in emails, social media, and phone calls are used to understand customer needs and wants as well as buying behavior and personalities.

- Human resources – HR uses data obtained from social media or mobile apps to discover characteristics and personalities when looking for potential employees. They also use the data to assess employee productivity. This means that it may no longer be necessary to take personality tests, as the collected data can be analyzed to check if a person matches the company culture and role for which he applies.

- Insurance and banking – understanding the risk profile of a customer applying for insurance or a loan, as the data is used to assess the client’s trustworthiness.

Datafication for Competitive Advantage

With the above use cases, it is evident that businesses can leverage datafication to help improve operations, thereby increasing productivity and revenue.

For instance, collecting real-time customer feedback can help improve products and services. Additionally, it becomes easy to determine and predict sales by analyzing data from social platforms such as Facebook, Instagram, and Twitter.

The information collected from social media, emails, and other digital platforms is then used to create personalized campaigns, effectively targeting the most interested audience.

How Businesses Can Implement Datafication

Any trending technology that presents benefits to a business comes at a cost. Luckily, cloud computing eases datafication for businesses as they don’t have to worry about acquiring necessary hardware and software. With readily available software as a service (SaaS) or platform as a service (PaaS) technologies, businesses need only to define the goal they want to achieve with the data collected.

The main concern of a business remains the proper implementation of datafication. To begin with, it is best to ensure that the right technology – such as mobile devices, voice assistants, wearables, and IoT – is used.

Next is to use appropriate platforms. Using the right platform will help effectively extract data that a business needs. Such platforms should also analyze massive amounts of data and produce reports that enhance decision-making.

Another critical factor is to have a centralized repository where all authorized people in the organization can access the data.

Finally, it’s crucial to have skilled professionals in data infrastructure, data management, and data analytics to evaluate and manage the data. This could either be an in-house team or outsourced.

Conclusion

Businesses that wish to remain relevant must consider datafication as part of their digital strategies. However, as datafication enters digital transformation, its successful implementation will require attention to data protection through adhering to legal requirements, technical measures such as access control, and best business practices.

5 QuickBooks Online Tasks You Should Do Before January 1

December always goes by so quickly. Seems like you’ve just finished Thanksgiving dinner and it’s time to ring in the New Year. You could probably spend the entire month on your personal obligations. But it’s also the end of the year, which means your busiest period if you’re a retailer. Even if you’re not, you probably have sales goals to try to meet. And you may have employee issues that need to be addressed before the calendar turns over.

On top of all of this, you should be closing out your books for the current year (as much as you can) in preparation for the new one. If you’ve been using QuickBooks Online conscientiously all year, your job will be a lot easier. But you’ll still need to carve out some time for year-end tasks.

We don’t expect that you’ll necessarily be able to wrap absolutely everything up by New Year’s Eve. You may be waiting for your customers and employees to do their part. But here are five things you can do amidst all of your other personal and professional plans that will help you get a jump on January.

Analyze your 2022 sales.

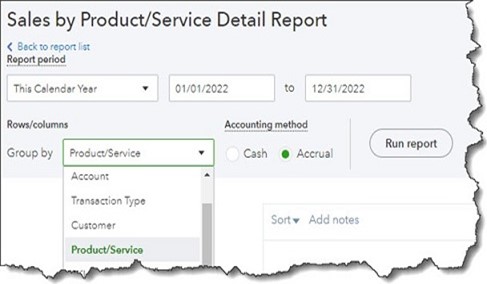

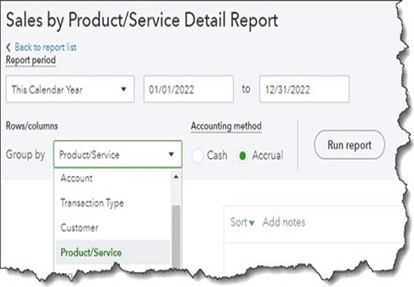

You won’t have your final numbers until the year is over, but you can get a good start in December. There are several QuickBooks Online reports that can give you a clear, understandable look at your 2022 sales. Click Reports in the toolbar and scroll down to Sales and customers. You can run reports that will tell you what your sales were by Class, Customer, Customer Type, and Product/Service, in summary or detail. The reports are customizable, so you can specify date ranges and group the results by, for example, Transaction Type, Customer, and Account.

You can customize and run QuickBooks Online’s Sales reports.

Warning: If you’re not clear about whether you should run reports in Cash or Accrual mode, let us help you with this. The distinction is important.

Know What You Owe

If money is tight at the end of the year, this will be a challenge. But you don’t want to come back from the holidays to a lot of past-due notices. To see what still needs to be paid, click Reports again and scroll down to What you owe. If you want the straight scoop right away, run Unpaid Bills. For a more detailed look, create the Accounts payable aging detail report. This groups your outstanding payables by days past due.

Know Who Still Owes You Money

This is a question that’s probably on your mind all year, but it’s especially important as the year winds down. It may be difficult to get delinquent customers to pay up in December, but you should at least know where you stand with them. Click the Reports tab again and scroll down Who owes you. Generate two reports there: Accounts receivable aging detail and Open Invoices.

You might also want to spend an hour coming up with some strategies that would encourage customers to pay faster. If you’re at a loss about this, we could sit down together and come up with a plan.

Create statements for past-due customers

Customer statements are something like reports. They display sales transactions within a given period. Statements can serve two purposes. Sometimes, customers just want a list of their invoices and payments for their records. You can also use statements as a reminder to customers who are past due on their accounts. Click New in the upper left corner, and then click Statement under Other. There are three types, but you’d be most likely to create and send two of them:

- Open Item. Displays all open, unpaid invoices for the last 365 days.

- Transaction Statement. Lists all transactions for the selected date range.

You can send statements to customers to remind them of overdue payments or just to provide a record of transactions for a given period.

Clean up your customers and vendor lists

If you only have a few of each, your list is probably current. But if you’ve been adding customers or vendors for years without ever editing the list, you’re probably spending too much time scrolling. You don’t have to delete them. You can just make them inactive. Click Sales in the toolbar, then Customers. If you know a customer has no open activity and you want to hide them, click in the box in front of the company or customer’s name. Repeat this for as many as you want, then click Batch actions in the upper left, then Make inactive.

A Busy Month

Don’t worry if you don’t get to all of these by the end of the year. But do add them to your January task list if you don’t. You might also consider having us run the standard financial reports that are available in QuickBooks Online Reports, under For my accountant. You can create reports like Trial Balance yourself, but they can be hard to analyze accurately. We’d be happy to set up a time after the first of the year to go over these after all of your 2022 transactions are in.

Tax Benefits for Holiday Family Employment

Along with the holidays comes a lot of extra work for many family-run businesses, which may require putting the kids to work and having a spouse help out over the busy time. There are special tax rules when hiring your children and also for your spouse, depending on whether he or she is a business partner or an employee.

Employing Your Child – Tax reform provided a more taxpayer-friendly tax treatment for children with earned income. Generally, when a child under the age of 19 or a student under the age of 24 without any investment income is claimed as a dependent of the parents, the child can earn up to $12,950 in 2022 without incurring any tax liability. If they earn more, then the next $10,275 is taxed at 10%. A reasonable salary paid to a child reduces the business-owner parents’ self-employment income and tax by shifting income to the child.

Example: You are in the 22% tax bracket and own an unincorporated business. You hire your 17-year-old child (who has no investment income) and pay the child $14,000 for 2022. You reduce your income by $14,000, which saves you $3,080 in income tax (22% of $14,000), and your child has a taxable income of $1,050 ($14,000 less the $12,950 standard deduction), on which the tax is $105 (10% of $1,050). Thus, the net income tax saved by the family is $2,975 ($3,080 − $105).

If the business is unincorporated and the wages are paid to a child under age 18, the wages will not be subject to FICA – Social Security and hospital insurance (HI, aka Medicare) – taxes since for FICA tax purposes, employment doesn’t include services performed by a child under the age of 18 while employed by a parent. Thus, the child will not be required to pay the employee’s share of the FICA taxes, and the business won’t have to pay its half either. In addition, by paying the child and thus reducing the business’s net income, the parent’s self-employment tax payable on net self-employment income will also be reduced.

Example: Expanding on the previous example and assuming your business profits are $130,000, by paying your child $14,000, you will reduce not only your self-employment income for income tax purposes but also your self-employment tax (the HI portion) by $375 (2.9% of $14,000 times the SE factor of 92.35%). But if your net profits for the year were less than the maximum SE income ($147,000 for 2022) subject to Social Security tax, then the savings would include the 12.4% Social Security portion in addition to the 2.9% HI portion.

A similar but more liberal exemption applies for FUTA, which exempts the earnings paid to a child under age 21 while employed by his or her parent from federal unemployment tax. The FICA and FUTA exemptions also apply if a child is employed by a partnership consisting solely of his or her parents. However, the exemptions do not apply to businesses that are incorporated or a partnership that includes non-parent partners. Even so, there’s no extra cost to your business if you pay a child for work that you would pay someone else to do anyway.

Additional savings are possible if the child is paid more or worked part-time during the year or in the summer and deposits the extra earnings into a traditional IRA. For 2022, the child can make a tax-deductible contribution of up to $6,000 to his or her own IRA. The business may also be able to provide the child with retirement plan benefits, depending on the type of plan it uses, its terms, the child’s age, and the number of hours worked. By combining the standard deduction ($12,950) and the maximum deductible IRA contribution ($6,000) for 2022, a child could earn $18,950 in wages and pay no income tax.

Example: Referring back to the original example, making a $6,000 traditional IRA contribution will only save the child $600 in tax, so it might be appropriate to make a Roth IRA contribution instead, especially since the child has so many years before retirement and the future tax-free retirement benefits will far outweigh the current $600 savings. Contributions to Roth IRAs aren’t deductible, but distributions are generally tax-free.

A child can benefit from the standard deduction and earn $12,950 tax-free (except FICA withholding) when working for someone else and still take advantage of an IRA deduction if his or her income exceeds the standard deduction.

For 2023, the standard deduction of a single person will increase to $13,850.

Note that if the child has unearned income, such as interest, dividends, or capital gains, and is under the age of 19 or is a student under the age of 24, the child may be subject to the “kiddie tax” rules, under which the tax on the unearned may be taxed at the parent’s tax rate. This situation is not covered in this article.

Husband and Wife Working in the Same Businesses – A spouse is considered an employee if there is an employer/employee type of relationship, i.e., the first spouse substantially controls the business in terms of management decisions and the second spouse is under the first spouse’s direction and control. If such a relationship exists, then the second spouse is an employee subject to income tax and FICA (Social Security and Medicare) withholding. However, if the second spouse has an equal say in the business’s affairs, provides substantially equal services to the business, and contributes capital to the business, then a partnership type of relationship exists and the business’s income should be reported as a partnership on IRS Form 1065 or as a qualified joint venture (see below).

While the income and expenses of a partnership activity are reported on Form 1065, the net income or loss of the business, as shown on Schedule K-1 from the 1065, will still end up on the partners’ individual 1040 return(s), to be combined with any other income the couple has for the year. Partnerships are sometimes referred to as flow-through entities.

A provision of the tax code generally permits a qualified joint venture whose only members are a husband and wife filing a joint return to not to be treated as a partnership for federal tax purposes. A qualified joint venture is a joint venture involving the conduct of a trade or business if:

(1) the only members of the joint venture are a husband and wife,

(2) both spouses materially participate in the trade or business, and

(3) both spouses elect to have the provision apply.

Under the provision, a qualified joint venture conducted by a husband and wife who file a joint return is not treated as a partnership for federal tax purposes. Instead, all income, gain, loss, deduction, and credit items are divided between the spouses in accordance with their respective interests in the venture. Each spouse takes into account his or her respective share of these items as a sole proprietor. Thus, it is anticipated that each spouse will account for his or her respective share on the appropriate form, such as Schedule C. When determining net earnings from self-employment for computing self-employment tax, each spouse’s share of income or loss from a qualified joint venture is taken into account, just as it is for federal income tax purposes under the provision (i.e., in accordance with their respective interests in the venture).

This generally does not increase the total tax on the return, but it does give each spouse credit for Social Security earnings, on which Social Security retirement benefits are based. However, this may not be true if either spouse exceeds the Social Security tax limitation.

If your spouse is your employee and not your partner, then you must make Social Security and Medicare tax payments to the government for him or her – half the amount comes from the employee via withholding from his or her wages, and half comes from the employer. The wages for the services of an individual who works for his or her spouse in a trade or business are subject to income tax withholding and Social Security and Medicare taxes but not to FUTA tax. In addition, state taxes may also have to be withheld and remitted to the state government. The employer-spouse must issue a Form W-2 for the employee-spouse.

If you have questions about the information provided here and other possible tax benefits or issues related to hiring your child or your spouse, please give our office a call.

Year-End Gift Giving with Tax Benefits

The holiday season is customarily a time of giving gifts, whether to your favorite charity, family members or others. Some gifts even provide a variety of tax benefits.

But be wary; during the holiday season, you may receive phone calls, texts, emails, snail mail, or appeals on social networking sites for donations for various causes. However, some of these appeals may come from fraudsters and not legitimate charities. Unfortunately, this happens every holiday season.

So, before writing a check or giving your credit card number to a charity that you aren’t familiar with, check them out so you can be assured that your donation will end up in the right hands. Follow these tips to make sure that your charitable contributions will actually go to the cause you are supporting:

- Donate to charities that you know and trust. Be alert for charities that seem to have sprung up overnight and that you are not familiar with.

- Ask if a caller is a paid fundraiser, who they work for, and what percentage of your donation goes to the charity and fundraiser. If you don’t get clear answers—or if you don’t like the answers you get—consider donating to a different organization.

- Don’t give out personal or financial information, such as your credit card or bank account number, unless you are sure that the charity is reputable.

- Never send cash. You can’t be sure that the organization will receive your donation, and you won’t have a record for tax purposes.

- Never wire money to someone who claims to be from a charity. Scammers often request donations to be wired because wiring money is like sending cash: Once you send it, you can’t get it back.

- If a donation request comes from a charity that claims to help a local community group (for example, police or firefighters), ask members of that group if they have heard of the charity and if it is actually providing financial support.

- Check out the charity’s reputation online using Charity Watch or other online watchdogs.

Gifts with Tax Benefits

A Gift of College Tuition – An interesting quirk in the gift tax laws is that an individual can pay a student’s higher-education tuitiondirectly to a qualified school, college, or university, and it will be exempt from gift tax and gift tax reporting. What student wouldn’t love to have part of their tuition paid? It would make a great gift. However, the giver isn’t allowed a charitable deduction on their income tax return for the tuition they generously paid.

As an aside, college tuition generally qualifies for a federal income tax credit. Another quirk in the tax laws says that the education credit goes to the individual who claims the child (student) as a dependent, generally resulting in a gift to the child’s parents in the form of the tax credit.

Example: Whitney is attending college and is the dependent of her mother and father. Whitney’s grandfather makes a tuition payment directly to the college; since it was made directly to the school, Whitney’s grandfather does not have any gift tax issues. Since Whitney is a dependent of her parents, her parents would claim any available tuition credit. Thus, by paying the tuition, Grandpa made a gift of tuition to his granddaughter and a gift of the tuition credit to her parents.

Qualified Tuition Program (Sec. 529 plans) – These arrangements allow taxpayers to put away large amounts of money, limited only by the projected cost of a college education, which varies from state to state with some plans capped at more than $525,000. The account’s earnings are tax-free if used to pay tuition and certain other college expenses, so the sooner the account is funded, the more it can earn. There are no limits on the number of donors or on age or income. The contributions are subject to the gift tax if the annual contribution exceeds the annual gift tax exclusion amount ($16,000 for 2022; $17,000 for 2023).

As of 2018, tax-free distributions of up to $10,000 per year per designated beneficiary are allowed for tuition (no other expenses are allowed) in connection with enrollment or attendance at elementary or secondary schools, including public, private and religious schools. However, this option should be considered cautiously, asSec. 529 plans work best when the money put into the plan is allowed to grow for a long period of time.

Qualified Charitable Distribution (QCDs) – Individuals age70½ or over can transfer up to $100,000 annually from their IRAs to qualified charities without the distribution being taxable. So, you might want to consider using QCDs for your smaller contributions. Contact your IRA custodian or trustee to arrange the transfer, which needs to be completed by December 31, 2022, to count for 2022. Since December 31, 2022 falls on a Saturday and is New Year’s Eve, it’s best not to wait until the last minute to initiate the transfer.

A word of caution:Congress, a couple of years ago, increased the IRA required minimum distribution (RMD) age to 72 but still allows QCDs once the taxpayer reaches age 70½, and they repealed the age restriction for making traditional IRA contributions beginning in 2020. This means a taxpayer can make traditional IRA contributions and QCDs after reaching age 70½. As a result, Congress included a provision in the tax law requiring a taxpayer who qualifies to make a QCD to reduce the QCD non-taxable portion by any traditional IRA contribution made after reaching 70½ that was deducted, even if the contribution and deduction are not in the same year. This is a complication you would want to consult this office about before making a QCD.

Donor-Advised Funds (DAFs) – If you would like to make a substantial tax-deductible charitable donation this year but spread the actual distribution of funds to specific charities over a number of years, a donor-advised fund may fill that need. There are any number of reasons individuals choose DAFs, including making a substantial charitable donation in an exceptionally high-income year.

A DAF is a separate fund (account) set up within a public charity to which a donor makes a contribution. The donor then advises the sponsoring organization on how to ultimately distribute the funds from the account as charitable gifts over the course of many years. The fund isn’t required to follow the donor’s requests, but most do.

Tax law allows the sponsoring organization to be independent, community-based, religiously affiliated, or connected with a financial institution. Minimum contributions typically range from $5,000 to $25,000. The sponsoring organization manages the administration of the fund and handles the tax reporting, usually for an annual fee of 1%.

You get to take a tax deduction for your entire donation in the year you contribute the funds or assets to the DAF. In addition, the funds that are not distributed are invested and grow until eventually being disbursed to the charitable organization(s).

Work Equipment – If your spouse is self-employed and you purchase tools or electronics used in your spouse’s business, the costs of gifts qualify as a business tax deduction on the return for the year when the equipment is put into service.

Gifts to Employees –It is common practice this time of year for employers to give their employees gifts. If a gift is infrequently offered and has a fair market value so low that it is impractical and unreasonable to account for it, the gift’s value is treated as ade minimis fringe benefit. As such, it would be tax-free to the employee, and its cost would be tax deductible by the employer. However, be cautious, as any amount of cash given to an employee must be treated as taxable wages.

Monetary Gifts to Individuals – If you have a high net worth, you are no doubt aware that when you pass away, your estate may be subject to federal (and possibly a state) estate tax once the value of your estate exceeds an excludable amount. With the passage of the Tax Cuts and Jobs Act (TCJA), effective in 2018, the estate tax exclusion amount was more than doubled, from $5.49 million in 2017 to $11.18 million in 2018. It has been inflation-adjusted each year since, so the 2022 exclusion amount is $12.06 million ($12,920,000 for 2023).

However, in case you have forgotten, most of the provisions of the TCJA are temporary and expire after 2025, at which time the estate tax exclusion will revert back to the pre-TCJA level. Estimating the inflation adjustments, the 2026 exclusion amount would be reduced to approximately $6.25 million. Any amount of your estate in excess of the exclusion amount will be subject to the estate tax, which currently has a top rate of 40%. If you are married, the estate tax applies to the second spouse to pass away.

The value of gifts you make to individuals during your lifetime reduces the estate tax exclusion amount available to offset the value of your estate when you pass away. However, the estate tax exclusion is only reduced when the gifts you make during life exceed an annual amount, which is $16,000 for 2022 and $17,000 for 2023. That annual exclusion applies per individual, meaning you can give up to the exclusion amount to as many people you’d like every year, whether or not they are related to you, without reducing the estate tax exclusion. Unlike gifts to qualified charitable organizations, gifts to individuals are not tax deductible.

Of course, depending which political party is in control in Washington, D.C. after the 2022 and 2024 elections, the lifetime gift and estate tax exclusion could be reduced before 2026, or could be extended or made permanent. Congress would need to agree to lower the exclusion amount or extend the higher amount.

Steps Your Business Can Take to Survive a Recession

According to one recent study, there is a 96% chance that the United States will experience some form of economic recession within the next 12 months. If you needed a single statistic to underline the importance of planning ahead when it comes to your business, let it be that one.

Thankfully, this news isn’t a guarantee of impending doom for your organization. Not only do businesses of all types survive recessions regularly, but some also manage to thrive. If you want to make sure that you’re as prepared as you can be for whatever the economy happens to throw at you, there are a number of important things to keep in mind.

Monitor Those Expenses

By far, the most important step that you can take to survive an impending recession involves locating places to cut spending whenever you can.

This is something that became particularly important during the economic downturn caused by the COVID-19 pandemic. With countless employees suddenly working from home indefinitely, businesses realized that they didn’t need massive offices or retail spaces anymore and used it as an opportunity to downsize.

Take a look at your recurring expenses, categorize everything into an order based on importance, and determine what you can live with and what you cannot. Along the same lines, use this as a chance to start re-negotiating any vendor contracts with terms that may not be as favorable as they once appeared.

Note that not only is monitoring your expenses not something that you “do once and forget about,” it should also be done often – even during those times when the economy is objectively strong. There are always areas that you can cut and trimming as much “fat” out of your expenses as possible is a perfect way to make sure that you remain protected even in the event of the unexpected.

Incentivize Cash Upfront

Another essential step you can take to survive a recession has to do with encouraging your clients to not only pay on time but to pay in cash upfront whenever possible.

To speak to the former, understand that most businesses deal with late payments regularly – but that doesn’t mean there aren’t steps you can take to mitigate the issue. If you haven’t already, switch to digital invoices and an electronic payment system to make it as easy as possible for people to pay you. Make sure that you know which invoices are outstanding and make follow-up phone calls to keep things moving.

In terms of collecting cash upfront, you could offer discounted prices and other incentives for people who are willing to pay now. Not everyone is going to take you up on that (as some might not be able to), but a lot of them will – allowing you to increase the amount of cash that you have coming into the business, making sure you have enough in reserves to help fend off a “rainy day” or two that may be coming.

Stay On Top of the Market

Finally, during uncertain economic times, it’s always important to make sure that you’re being proactive about staying up-to-date with the market itself – at least to the extent that you’re able to.

At a bare minimum, you need to regularly perform a market analysis to guarantee that you know exactly what is going on and that you’ve identified any pivots that must be made in the short term. To continue to use the example of the COVID-19 pandemic, this was a period where consumer buying patterns and behaviors changed dramatically in a short window of time. Those organizations who insisted on pushing along as if nothing had changed tended to be the ones that suffered. Those who were able to understand these changes and make quick adjustments with their own efforts were able to make the most of it.

Likewise, read the news and make sure you’re aware of what the projected impact of such a recession is likely to be. Right now, things are still far enough away to where nobody really knows what might happen – just that something is (likely) coming. When that recession actually does arrive and the economy begins to detract, things can shift quickly. By staying in the loop about the larger economy, you have the actionable information you need to make more informed decisions on a day-to-day basis.

In the end, no business owner wants to deal with the impact of a recession – but that doesn’t change the reality of the situation. At some point, you are likely to find yourself in this situation and taking the appropriate steps today can help avert a potentially larger issue tomorrow.

If you’d like to find out more information about the steps that your business can take to survive a recession, or if you’d just like to discuss your own needs with someone in a bit more detail, please don’t delay – contact us to speak to a professional today.

Your Year-End Financial Checklist

Believe it or not, the year is coming to a close. If you want to finish strong and set attainable goals for 2023, here’s a handy, actionable checklist to help you navigate upcoming expenditures.

Review Your Spending and Create a Budget

This might seem like Finance 101, but it’s a tried and true method that works. Take a look back to see where your money went. When you’ve evaluated your patterns of spending, you can reset priorities for the New Year, assuming you want to make changes. If you do, sit down and create a budget. Your tax professional will probably have a downloadable tax planning guild so ask them first, but here’s an example of a family-friendly free, downloadable template to get you started on your 2023 plan.

Rethink Your Savings

If you already have a healthy amount in savings, congrats. Make sure it’s an account that’s interest-bearing and you have the best rate. However, if you had to dip into your emergency savings, then chart a course to replenish it. If you don’t have an emergency fund, it makes good sense to start one. A smart rule to consider is having six months of income saved up, should your heater go out, you experience a sudden job loss, or suffer unforeseen medical expenses that your insurance doesn’t cover. A no-nonsense way to begin is to automate a certain amount each month that will be deducted from your paycheck. You’ll begin to accumulate money in no time. Best of all, you’ll never miss it.

Evaluate Your Debt

Have you made progress in paying it down? Or have you gone the other way? If you’ve eliminated your debt, once again, congrats. If you’ve increased your debt, don’t despair because there are some easy ways to cut expenses. Slow down on eating out. Review your subscriptions and see which ones you really need. Here’s a list of more areas to consider. Another way to get rid of the shackles of debt is to apply for a consolidation loan. You might also use the debt snowball method—starting with the smallest debt and working your way up to the largest. Or the inverse, the debt avalanche, where you pay off high-interest rate balances first.

Contribute to Your 401(k) by Dec. 31

You still have time to do this, but make sure it happens before the clock strikes midnight on Dec. 31. If you’re fortunate enough to receive a year-end bonus, you might want to put as much of it as you can toward your 401(k) plan. For the New Year, increase the amount you’re contributing. Just one or more percentage points higher can make a big difference. Finally, if your company offers a match that you have yet to take advantage of (read: max out), do so before it’s too late.

Consider a Roth Conversion

If you’ve experienced a loss of income this year, you may be in a lower tax bracket. This means you can take advantage of your situation by converting some of your pre-tax assets like a Traditional IRA into a Roth IRA. If you’ve earned too much to convert to a Roth IRA, a back-door Roth IRA contribution might be the way to go. Here’s how you do it: Deposit money into a non-deductible Traditional IRA, then convert that IRA into a Roth IRA. But before you do anything at all, consult your tax advisor, as there are potential costs and tax liabilities that might come up.

Check your FSA Balance

An FSA (Flexible Spending Account) is a great benefit if your employer offers it. However, check your balance to see how much you have left because the rule is: Use it or lose it. That said, many companies offer a grace period until mid-March to spend what you have left, though not all do. Make sure to inquire about the rules of your account before the New Year.

Get a Free Credit Report

When was the last time you checked your credit? If you haven’t done so, now’s a good time because looking back can help you plan ahead. Here’s a great place to get a free report. If you notice any errors or discover any identity theft, you can immediately take steps to correct them and start with a clean slate for 2023.

While taking care of financial matters at the end of the year can be a love/hate kind of thing to do, if you spend a little time now, the coming days might be substantially merrier and bright.

Sources

https://www.bankrate.com/personal-finance/end-of-year-financial-checklist/

https://www.fundingcloudnine.com/budget-cut/

https://www.bankrate.com/retirement/what-is-a-backdoor-roth-ira/

End of Life Planning: 5 Steps to Take in 2022

End-of-life planning is a delicate—but incredibly important—subject. While contemplating your own death and the fallout thereof probably feels morbid, making preparations for your passing is an incredible way to demonstrate your love to those near and dear to you. Taking the time to plan for some of the logistical details surrounding your death can go a very long way in lightening the heavy load that your loved ones will bear.

Whether you already have your end-of-life plan established or you have yet to do so, there is still work to do. Today we want to address 5 key areas that you should examine in 2022 in order to establish or strengthen your end-of-life plan.

1. Incapacitation – Your desires regarding how healthcare decisions are made in the event of your incapacitation

To establish, partner with an attorney to create your living will. Be sure that you establish power of attorney with a loved one in the event of your incapacitation.

To maintain, review your living will and update your power of attorney to reflect any changes

2. Inheritance – Your plan for how your valued assets will be passed on after your death

To establish, once again, find an attorney who is well versed in estate law. Work with them to create your will.

To maintain, review the will that you have already created, updating it for any major life changes that have bearing on it. Some examples of important changes that might require updates include an increase in your wealth, the birth or death of a loved one, or new marriages or divorces.

3. Information – A record of your papers, accounts, passwords, and more

To establish, make a thorough record of all of the key information that your loved ones and/or legal representatives might need after you pass on. This includes personal information, family information, important contacts, the location of important papers, funeral and interment details, obituary information, login and password information, social media account information, copies of important documents, and more.

To maintain, review the record that you have created and make any changes required to maintain its accuracy and relevance.

4. Dependents – Your plan for the continued care of any minor children, adult dependents, and/or pets

To establish, make a thorough plan that covers the care of any and all dependents that your death or incapacitation would leave hanging. It is best to work with an attorney in order to make sure all of your bases are covered.

To maintain, review the dependent care plan that you have already created, updating it for any major life changes that have bearing on it. Consider checking in with any individuals whom you have named to care for your dependents to make sure that they are still willing to be included in your plan.

5. Tax Planning – Your strategy for minimizing the taxes and expenses associated with the passing on of your estate

To establish, regardless of the size of your estate, having a clear plan in place is an important part of end-of-life planning. There are a number of key financial planning steps you can take in order to make the burden that your loved ones will carry as light as possible. We strongly recommend working with a tax accountant to make a thorough plan that minimizes the taxes and expenses that your loved ones will face in the event of your death.

To maintain, be sure to review your plan with your tax advisor on a regular basis in order to make sure that it is still optimized for your situation.

Taking the time to make and maintain a thorough end-of-life plan is one of the best gifts you can leave your loved ones upon your passing. It is a hard topic to address, but an incredibly important one.

Though this article offers some helpful tips and starting points, the best way to create a thorough and effective end-of-life plan is to work with a professional who can guide you each and every step of the way. If you are ready to take this important planning step, reach out to the RBG professionals today. You can do so via our website’s Contact page or by emailing rbfco@rbfco.com. Be sure to request a copy of our free “Everything They Need to Know” digital planning guide.

Department of Revenue Launches New Online Tax System for PA Businesses

On November 30, the Pennsylvania Department of Revenue launched a new online system for business taxpayers. myPATH, which has been available to individual taxpayers since June 2022, replaces e-TIDES as a full-service system for business taxpayers to handle their registration, filing and payments. The new platform is user-friendly and designed to be responsive to computers, mobile phones, and tablets.

Business taxpayers will be able to use myPATH to manage a number of taxes, including withholding tax, sales tax, and corporation tax. myPATH also replaces Pennsylvania Online Business Entity Registration (PA-100), which was an online platform previously used by businesses to register for state taxes.

As part of the transition to myPATH, business filers need to create a new account. Instructions for this process can be found here. Once logged in with their new username and password, customers have the option of migrating their existing credentials from e-TIDES, which will allow them to access their prior account information.

For more information about business taxpayers’ transition to myPATH and the state’s tax system modernization project, read the full press release from the Department of Revenue here.